After enjoying years of strong growth fueled by the commodity super cycle, many Sub-Saharan African (SSA) economies have more recently seen growth slow materially, at the same time experiencing declining foreign direct investment and rising budget deficits. The collapse of commodity prices, tighter international financing conditions, and unfavorable weather across parts of the region all contributed to regional GDP growth falling to around 2.2% in 2016, the slowest pace in over a decade. That said, IMF forecasts suggest that the region will still remain the world’s second-fastest-growing!

From our local perspective, we continue to believe that whilst the headlines may talk of slowing growth, there remain pockets of under-appreciated opportunity, particularly in Francophone SSA where some economies are still growing at an impressive annual rate of over 5%.

Why is Francophone SSA an attractive investment opportunity?

Selected diversified economies in Francophone SSA with limited dependence on commodities are emerging as the “winners” …

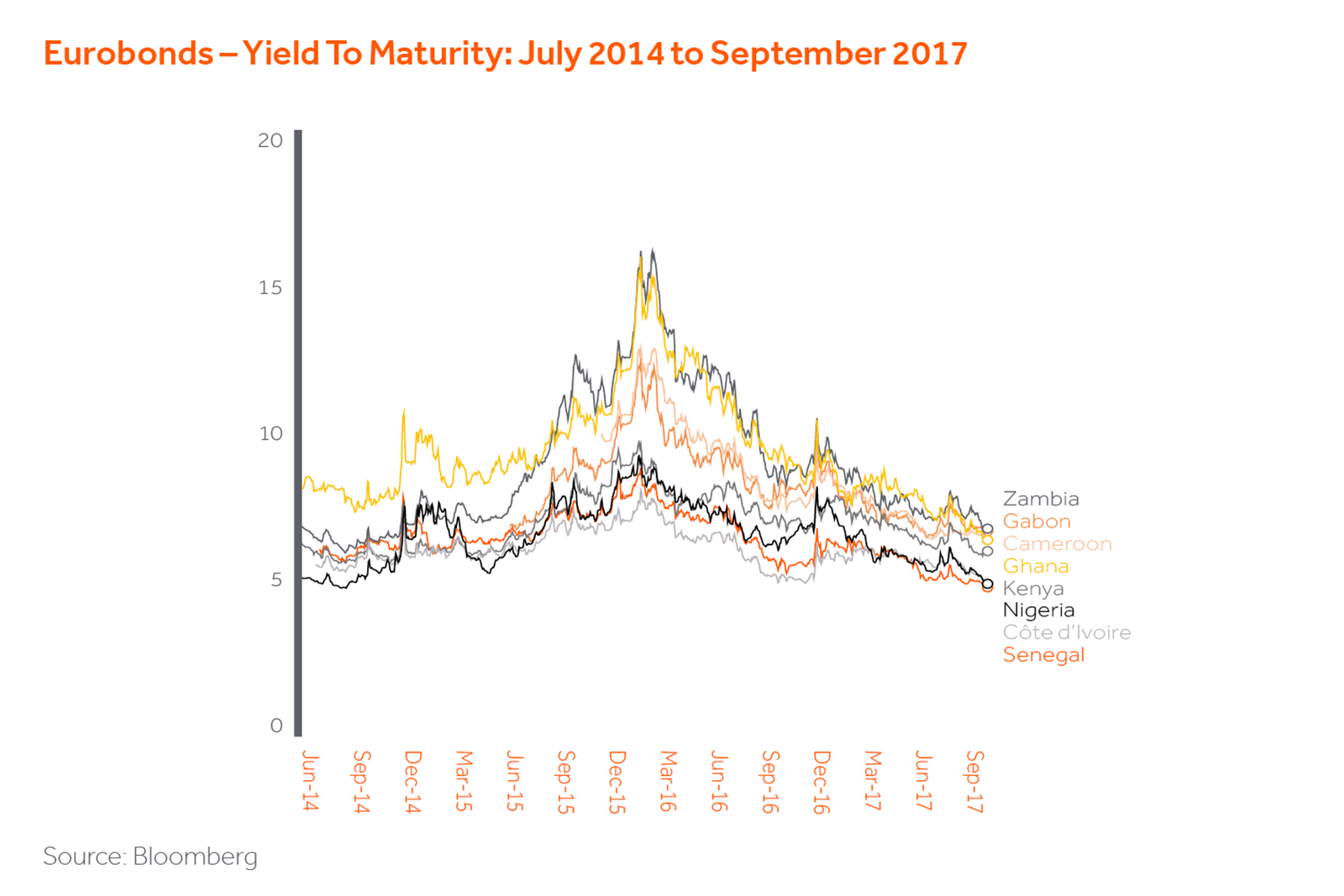

The Africa Rising narrative that fuelled investor confidence in the period immediately following the global financial crisis has proven to have multiple speeds, with the biggest winners seeming to be countries located in West Africa (Exhibit 1) that have limited exposure to oil and where weather conditions have been conducive to agricultural sector growth.

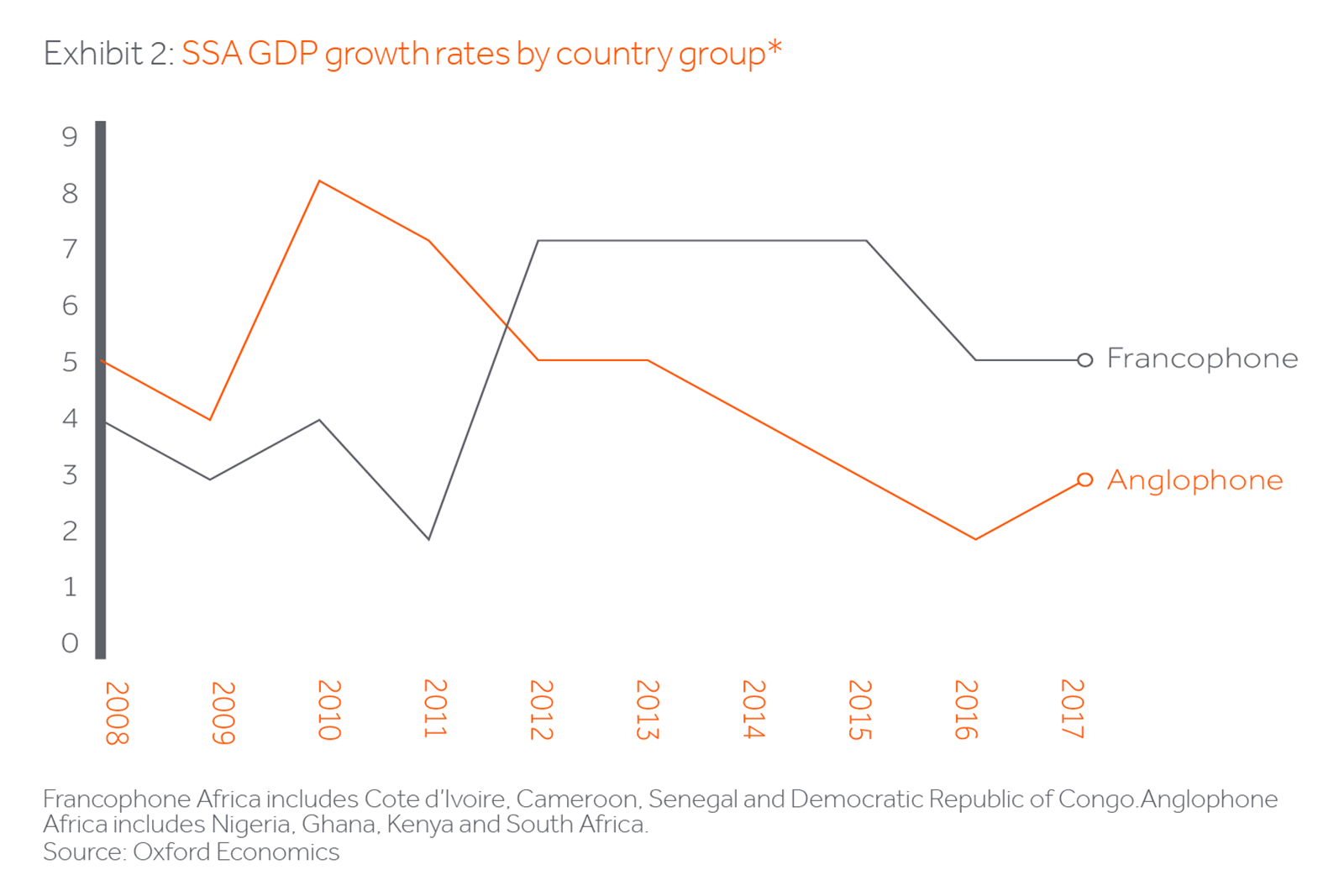

And real GDP growth for some of them has been among the fastest in SSA…

In particular, Cote d’Ivoire and Senegal have both seen GDP growth data for 2015-16 revised upwards by the IMF. Cote d’Ivoire has probably been the star-performing economy of SSA in recent years, with growth averaging 7% in the three years 2014-16. (exhibit 2). Cote d’Ivoire is recovering after a decade lost to a political crisis. Its current growth is supported by an emerging middle class, robust infrastructure development and an improved business environment. Arguably starting from a low base has helped maintain the growth momentum in Ivory Coast in recent years, but the government has also been using high levels of public investment to drive economic growth. This is changing as there are now signs that the government is changing tack and trying to encourage new private sector investment. Senegal is experiencing its highest growth rates in more than a decade because of rising investment flows while Cameroon’s economy is expected to remain fairly resilient in 2017, growing at around 5%, supported by a relatively well-diversified economic base, low debt ratios and the CFA (Communauté Financière Africaine) franc membership.

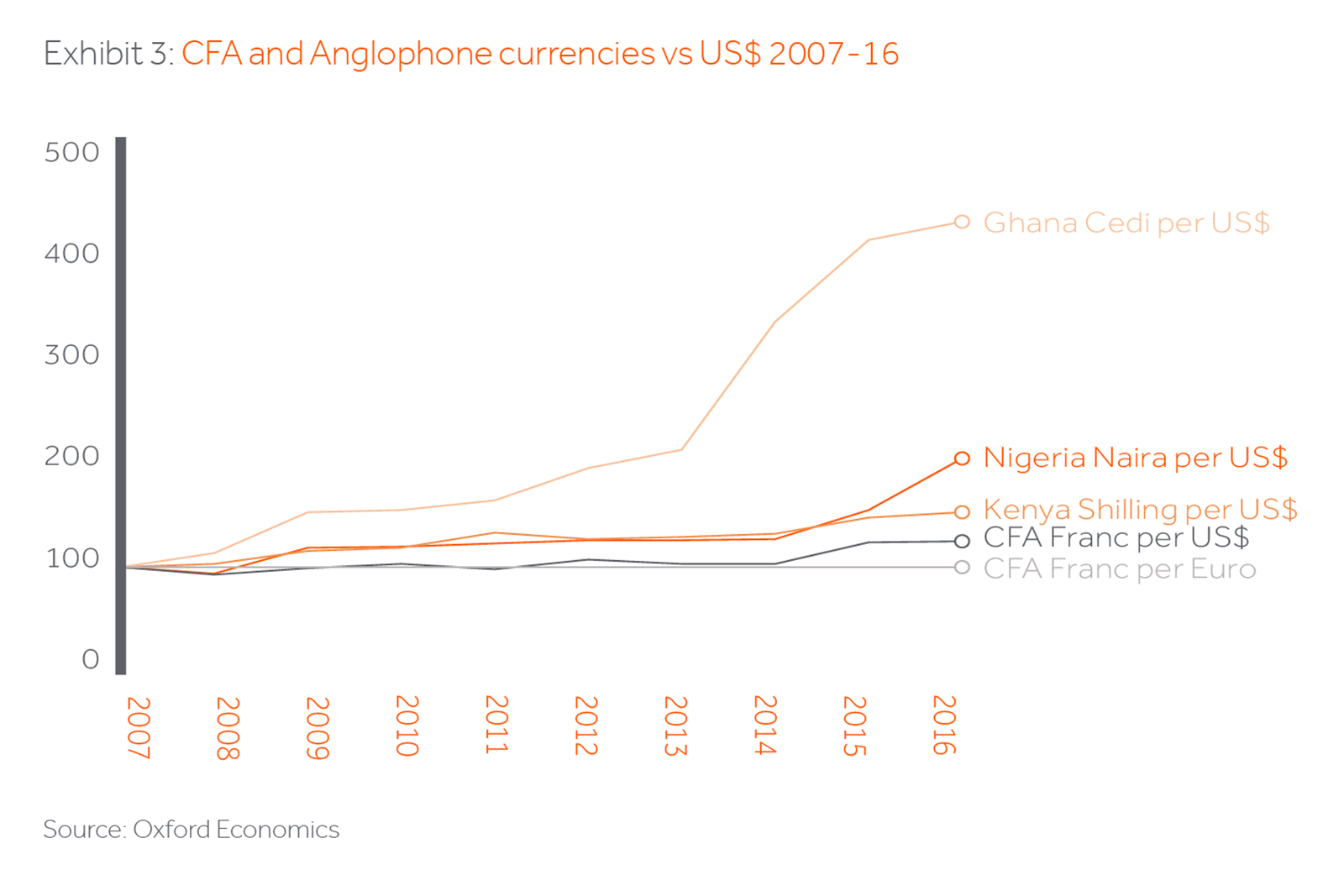

In addition to growth, the region benefits from reduced currency risk and structurally lower inflation.

The shared CFA franc is arguably the most important differentiator for the region, mitigating the high FX volatility seen in other SSA countries (Exhibit 3). The currency is pegged to the euro and used by over 150 million people and is the only single currency system in Africa. The IMF expects headline inflation for Francophone SSA to remain below 3% this year.

The CFA Franc Zone (Exhibit 4) currently comprises a group of fourteen francophone African countries that developed after the colonial era. After achieving political independence from France in the late 1950s and early 1960s, these nations chose to retain close economic links with their former colonial ruler. Africa’s franc zone is made up of two economic blocs, the Union Economique et Monétaire Ouest-Africaine (UEMOA) and the Communauté Économique et Monétaire de l’Afrique Centrale (CEMAC). The two unions roughly correspond to administrative boundaries within the former French colonial empire. Each bloc has its own regional central bank which issue a single currency pegged to the euro at the same rate (655.957/EUR) but the two units are not interchangeable. The two unions’ monetary policies are set by regional central banks, and the convertibility of the currency is guaranteed by the French treasury.

Although growing faster, the region is still receiving low foreign capital inflows allowing the first-mover to achieve advantageous returns.

One of the basic propositions for the Francophone SSA investment case is that it remains one of least penetrated regions in terms of investment flows. For reasons that do not always seem logical, investors interested in SSA have long preferred to focus on Anglophone Africa and particularly on commodity-rich countries. Understanding the opportunity in Francophone SSA has seemed to present more challenges. In private equity, of the US$5.4bn worth of investment into West Africa over the past six years, 64% was invested in Nigeria, 29% in Ghana and just 2% went to Cote d’Ivoire, and less than 1% flowed to every other country in the region. The evidence of under-investment in the region is to be seen everywhere on the ground, and as Warren Buffett famously advised “Be fearful when others are greedy. Be greedy when others are fearful.” At Actis, we believe our local presence and understanding gives us good reason to appreciate the risks but also to invest where others may fear to tread.

In the real estate sector, there are currently no institutional grade office buildings in Abidjan, the capital of Cote d’Ivoire, and multinationals firms looking to enter the region are forced to refurbish buildings built during the 1970’s or convert residential property, with both often failing international health and safety standards. This in a city which in the 1970s was referred to as the “Manhattan of Africa”. Our launch of the new Renaissance Plaza office development on a prime site in central Abidjan will see an iconic tower appear on the skyline in 2019 (Exhibit 5). In addition to opportunities in the office sector, the increasing formalization of the retail market, coupled with the shortage of A-grade retail and office stock and strong tenant demand has also created an opportunity to develop international mixed use assets in these markets.

In addition to growth, the diversification of some economies and the peg of the currency to the Euro, the region has a number of other attributes that make it a particularly attractive destination for foreign investors on the continent: Favorable demographic trends, improving institutional landscape, comparative advantage in natural resources just to name a few.

Business opportunities in Francophone SSA are potentially very large, particularly for companies in consumer-facing industries such as retail, telecommunications, banking and infrastructure. Several urban regions in the Franc Zone are emerging as consumption hubs. Cities such as Kinshasa, Abidjan, Douala, and Dakar are becoming increasingly attractive for investors looking to invest in high growth diversified economies with a strong consumer base and growing purchasing power.

How far is Francophone SSA from transitioning to ‘Emerging Market’ status?

Although Ivory coast, Cameroon and Senegal and other governments in Francophone SSA have all adopted a new development model to accelerate progress towards becoming emerging economies as well as a business hub for their respective region, governments in the region need to greatly up their game and pay due attention to correcting policy and generally creating a climate attractive to business, including foreign investment.

The years of high commodity prices may be unlikely to return soon, but if governments in Francophone SSA learn the lessons of the post-commodity crash, and continue their diversification with investment in infrastructure, encouraging the growth of the consumer goods and services sectors, including tourism, and bolstering financial services and telecoms through improvements in overall governance and the business climates, we expect more investors to follow our lead accelerating the transition of the region to a more mature capital market status.