Latin America will face an unusually busy election season this year. All but one of the five largest economies in the region will renew their president, with eight elections taking place in total (seven if we do not count Venezuela’s attempt). Chile kicked off the cycle in late 2017 and Colombia, Mexico and Brazil will follow over the next few months. Economies producing over $4 trillion in GDP, around 70% of the region’s total output, will change leadership. By the end of the year, two out of every three Latin Americans will have a new president. Even football is taking a secondary role in the news.

The elections take place at a time where the environment is strongly defined by two factors. The first is a marked increase in public anger over corruption, amid a plethora of scandals that initiated in Brazil and Central America and spread from Patagonia to Tijuana, holding to account previously untouchable figures including heads of state. Second, and related to the prior point, is a sense of disillusionment with democracy across the region, affecting the credibility of traditional parties and politicians.

There are parallels with the political rearrangement in the developed world. The feeling of disenchantment is giving rise to political outsiders riding the mood. These candidates are coming from across the political spectrum, running more on a banner of change from the establishment, as opposed to a unified policy wave similar to the “pink-tide” movement observed in Latin America in the 2000’s.

The stakes for Latin America are not small. The region has tracked the commodity slump and recovery, which affected many of its economies over the last 3 years. Asset prices have followed: between mid-2015 and the end of 2017 the MSCI LatAm index rose by over 50%. The political sphere has also experienced a shift toward the center-right, with recent elections in Argentina, Peru and Chile counteracting the move towards the left of a handful of economies over the past decade.

Purging corruption would certainly be a windfall for the region. It is one of the longest lasting endemics in Latin America, with a tangible effect on private investment. But a sudden and aggressive backlash comes at a cost. The scandals have held back economic activity, disrupted the political order and polarized the electoral landscape. Extricating the issue while maintaining a functioning political system is the key balance to strike. The role of strong institutions, an independent Central Bank and adequate governmental checks and balances, already well-established in most major Latin American economies, will be crucial in navigating this transition.

The overall trend points to a welcome deepening of the democratic system across Latin America. For the first time in a major election cycle, the majority of the voting population is now part of the growing middle class, as opposed to living in poverty. This will make room for a continually more pragmatic and educated population, one that is less suggestible and ideologically influenced. The decision will be theirs to drive the next wave in Latin American politics.

We now dive more deeply into the election cycle in Brazil and Mexico, Latin America’s two largest economies and major investment destinations for Actis, to offer a view of how the elections are seen from the street.

Mexico

In a widely sweeping electoral event, Mexicans go to the polls on 1 July to elect their President for the next six years, as well as to fill over 3,000 seats at the federal, state and municipal level. In unison with the regional thematic, elections take place at a time where demand for change is the main driver of decision making at the ballot box.

Looking at the data from afar, a desire for change feels unwarranted. The macro backdrop is decidedly strong. Unemployment is at historic lows, inflation is controlled and the economy is growing steadily, albeit moderately, on the back of a strong US economy. Additionally, NAFTA appears to be moving in the right direction despite occasional setbacks on the global trade stage, most recently at the G7 summit, and delays imposed by the US electoral calendar.

However, a deeper dive shows Mexicans feel much better about their personal situation than the direction of their country. Topping the list of concerns is generalized frustration with shortcomings in the rule of law, corruption and security. In conjunction with what is being observed in the broader region, voters are exhibiting a new set of priorities beyond just the economy and financial stability.

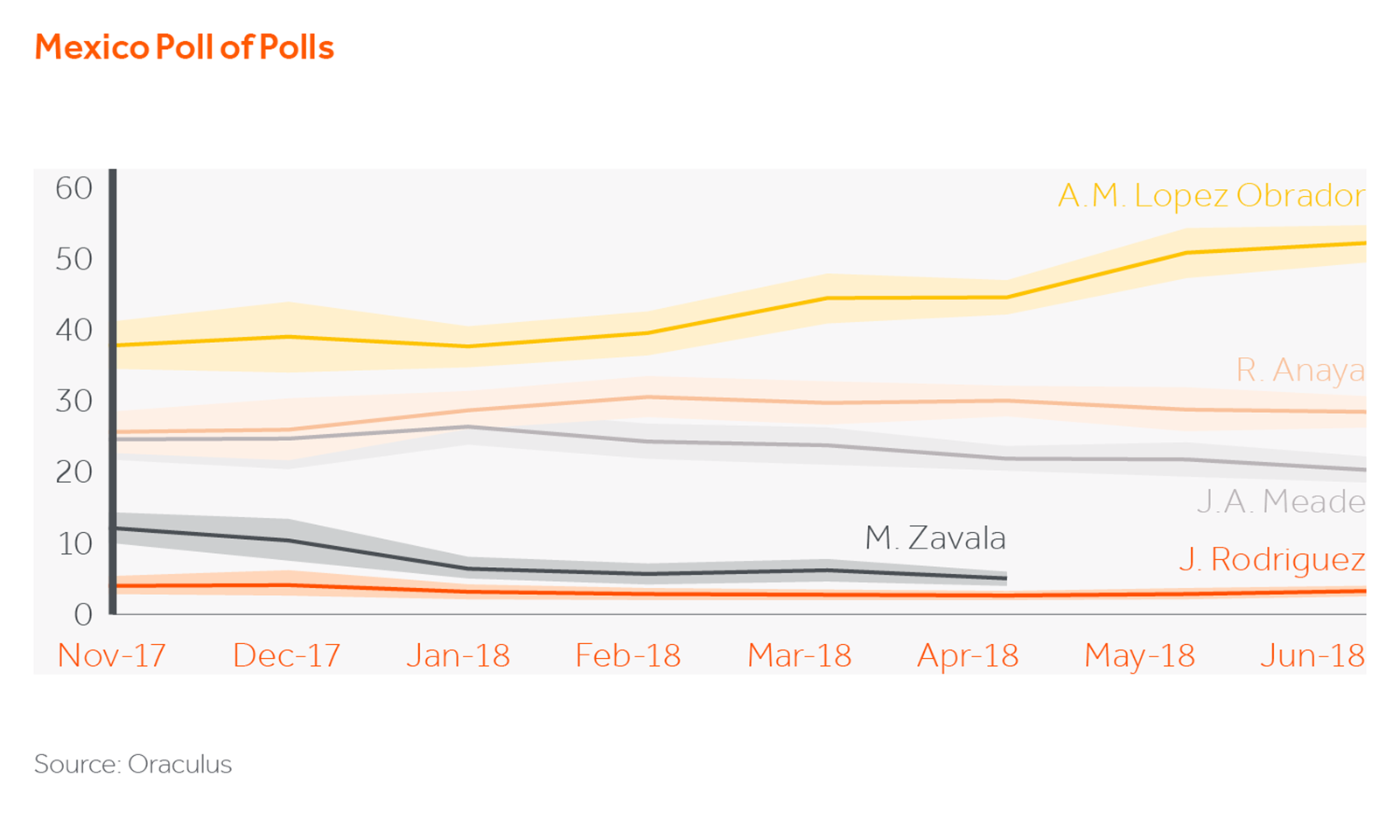

Andres Manuel Lopez Obrador (a.k.a. AMLO), the left-leaning candidate running for office, remains comfortably in the lead with most polls attributing a probability of over 90% to his winning. However, a large undecided swath of the vote (c. 20-30%) and recent electoral history show that poll results can quickly tighten or reverse by election day, making this a race to observe through to the end. Hurt by the unpopularity of traditional parties and the desire for change, his contenders, Jose Antonio Meade of the incumbent PRI party and Ricardo Anaya from the conservative PAN party, have not been able to shake each other off to consolidate a second place position to contend AMLO.

So, who is AMLO? For the first couple of decades in his regional political career, AMLO came up as part of the incumbent PRI party, splitting off with its more left-leaning faction, the PRD, in the late 1980’s. He progressed as a party leader, yet has only held public office once as Mayor of Mexico City in 2000-2005. Alongside his progressive social agenda, he espoused restructuring municipal debt to keep the deficit in check and implemented significant infrastructure projects, leaving office with one of the highest approval ratings in recent history. Since then, he has been unsuccessfully dedicated to running for President on an anti-establishment platform. This is his third attempt after coming close to victory in 2006 and attempting again in 2012.

Three main factors have helped this time around. The first has to do with the unpopularity of the traditional PRI party, currently led by President Enrique Pena Nieto, crippled by corruption allegations and security concerns. The PRI has had a near monopoly on power for nearly a century, only interrupted by two PAN party presidencies in 2000-2012, after over 70 years of PRI rule. The duopoly has been breaking at the seams over the past twenty years, with this election looking like the potential final blow. The second factor has to do with the more moderate tone adopted by AMLO’s campaign vis-à-vis his prior attempts at office. The script includes job creation, growth, lower spending and progressive fiscal reform while seeking open conversation with the private sector and relatively technocratic cabinet nominations to assuage concerns. Finally, the Trump administration’s more adversarial role on commerce and immigration have provoked an openness to more nationalistic views in the context of a country that is today one of the most outward looking in the world (e.g. Mexico holds the most free-trade agreements globally).

The election comes at an important juncture. Consolidation of positive adjustments to strengthen Mexico’s fiscal position, continuity of structural reforms, and consummation of a NAFTA 2.0 deal will all be strategic drivers for Mexico’s growth path in the next decade. At the same time, a new leader will need to attack corruption and tend to the security issue near the US border. Arguably, for the first time in its modern history, Mexico will need to address these important matters in the context of political discord. A government majority that speaks in concert on most policy fronts will be a thing of the past. Morena, AMLO’s party, will become a relevant force in Congress, living alongside the more traditional PRI, PAN and PRD parties. The risk though, looks more weighted towards legislative gridlock as opposed to drastic policy U-turns. The role of Mexico’s strong institutions will take center stage in successfully navigating through this process.

Postscript: As investors and portfolio managers, there are key tactical considerations to keep in mind around the election, both in the short and medium term. More immediately, we expected to see volatility in the FX and rate markets in the months leading up to elections, just as had been observed in the 2006 and 2012 election cycles. Both of these have materialized, with the Peso devaluing by c. 12% against the US Dollar over the past quarter and spreads widening, exacerbated by a global emerging market sell-off that has affected other emerging market currencies. In anticipation of this, we sought to close the acquisition-financing bond offering for our Saavi Energia acquisition ahead of this window. The team successfully funded the transaction straight into the bond, closing the financing one week ahead of the share transfer in April, anticipating the expected market volatility. Second, we could expect to see a temporary slowdown in investment pace related to new electricity auctions in the first year while the government transitions. We have sourced proprietary M&A and sector consolidation opportunities which are coming to us on the basis of our track record in market and could make up for a potential lull during this period. In the longer term, the investment proposition remains robust and aligned with our global energy strategy. Our focus is on enabling win-win scenarios for all stakeholders by investing in leading power generation companies that provide cost-efficient, clean and reliable electricity. All these are desired energy policy characteristics for any incoming government.

Brazil

On October 7th Brazilians will head to ballots to elect a new president for the next 4 years, a period that will be instrumental for the country’s stability from economic and social standpoints. However, the upcoming election brings a set of unique characteristics and understanding how this can affect the results in October, will help the reader digest the news popping up daily.

By contrast with the 2014 presidential election, political reform has introduced new conditions limiting campaign funding and time allocation for electoral advertisement on TV. Candidates have an expenditure cap (R$70m for presidential election and, if necessary, additional R$35m for run-off candidates) and will no longer count on corporations to fund their campaigns, having only two alternatives to raise funds:

- Individuals, with a cap of 10 minimum wages, and

- Federal state funds of c.R$2.5bn, proportionally distributed to parties following their representatives in the Lower House and Senate.

Unsurprisingly, parties from the establishment such as MDB (current president Michel Temer), PT (former presidents Dilma Rousseff and Luis Ignacio “Lula” da Silvia) and PSDB (former president Fernando Henrique Cardoso) are the largest recipients from such funds. Following the same rationale, the advertisement time on TV will also be allocated according to the relevance of each party measured by the seats each party secured in the Lower House 2014 election.

Whilst MDB, PSDB and PT remain the leading parties in terms of funds and television time, the boundaries imposed by the political reform represents a watershed in Brazilian presidential campaigns by limiting spending and airtime. Moreover, the growing importance of social media in a country where two thirds of the population have access to internet, including 130 million Facebook users (4th country in quantity of users) and 120 million on WhatsApp is a game changer. Candidates with limited budgets are using social media to boost their profile. Jair Bolsonaro and Marina Silva, from hitherto fringe parties have the largest number of followers on Twitter and Facebook.

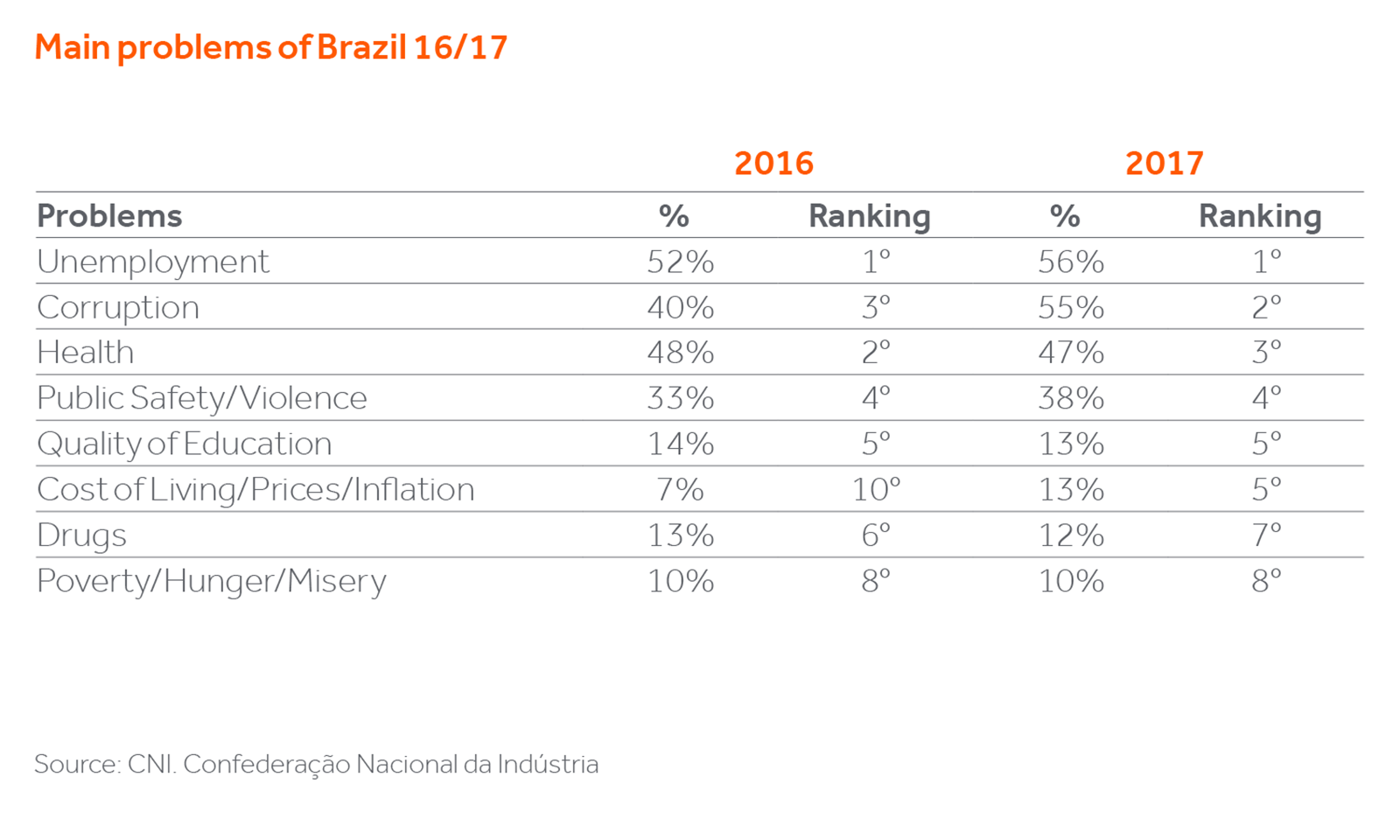

From a social standpoint, the corruption scheme unveiled by the Lava Jato operation has changed the political landscape. Fighting corruption has become one of the most important demands from Brazilian voters, followed by healthcare, security and education.

Additionally, the population shows a lack of confidence and credibility in establishment candidates, mirroring other LatAm countries and mature economies such as US, France and Italy. Notwithstanding this, some particular features remain. According to recent polls the majority of the voting population can be considered more conservative in terms of social values (leaning towards right-wing candidates) which changes when compared to economic policies, favoring greater government intervention, especially on issues related to the labour market and government support, to private corporations in distress.

On the economic front, structural reforms to stabilize the fiscal deficit and boost productivity remain essential. Public debt at 75% of GDP, is high by EM standards. The primary surplus partially offsets substantial public expenditures, mainly on social security which if unaddressed will see public debt rising to over 90% of GDP in the next 2-3 years. Essential investments in infrastructure are needed, mainly in logistics and energy, yet local sources of funding such as development banks lack capacity. Foreign capital is needed to bridge the funding gap but the lack of structural changes may impact the ability of the country to attract long-term investment capital.

The combination of campaign spending reforms, social media impact and the demands from Brazilian voters seem to favor new leadership. Despite the center-left preference of Brazilian voters in terms of social values, the new President will need to approve the structural reforms to put the country back on track, stabilizing inflation and bringing GDP sustainable growth. Therefore, the ability in building consensus will be key, mainly in an election where Brazilians will also vote for two-thirds of Senate and Lower House representatives.

Remember, Brazil is not for beginners. The months before presidential elections tend to introduce more volatility in the local capital market. This time, both external and domestic factors are contributing to this.

Locally, after being accused of corruption, Mr. Temer lost credibility and ability to pass reforms and spent the last few months fending off accusations. More recently, a truckers’ strike nearly halted the country for a week, culminating in the resignation of Petrobras’s CEO, exposing the weakness of Mr. Temer and his cabinet, and suggesting that the transition period until the next president takes the office won’t be as smooth as expected.

Externally the combination of US rate rises and tightening funding conditions have buffeted weaker emerging market countries. Whilst we believe this is a passing phase it is the more vulnerable economies which are bearing the strain as we report elsewhere (page 3).

The Brazilian Real has depreciated by c. 11% since the beginning January, being currently traded around 3.70-3.80. Following the currency over-devaluation, the Central Bank has carried out a full roll-over of FX swaps, increasing FX swap inventory to $42bn, until elections in October it may surpass $100bn. The investment pace is also slowing down with foreign and institutional investors taking a more bearish approach that contributed to IBOVESPA index loosing c.15% in LCY over the last month.

In the fixed-income market, the slope of interest rate (CDI) and sovereign bonds yield have moved upwards, interest rate expectation for January 2020 increased by 78 bps and sovereign bonds yield for the same maturity, 112 bps. The beginning of official campaigns in August tend to shed more light on this scenario to the extent that candidates will present their governmental proposals – heightened volatility may persist throughout 2H18 being impacted by the quality of the programs as well as the result of polls but, the investment community will be reacting in a more structured rather than speculative way.

Understanding the Brazilian puzzle is key. Brazil has 35 registered political parties whilst for this upcoming presidential election 17 pre-candidates announced intentions to run. This number will certainly decrease, as the official candidacies are only due by August 15th and alliances may be structured, decreasing the number of official candidates. This current presidential election presents a level of fragmentation last seen in 1989; back then Luis Ignacio “Lula” da Silva went for the run-offs with only 17% of valid votes, when he ended up losing to Fernando Collor de Mello.

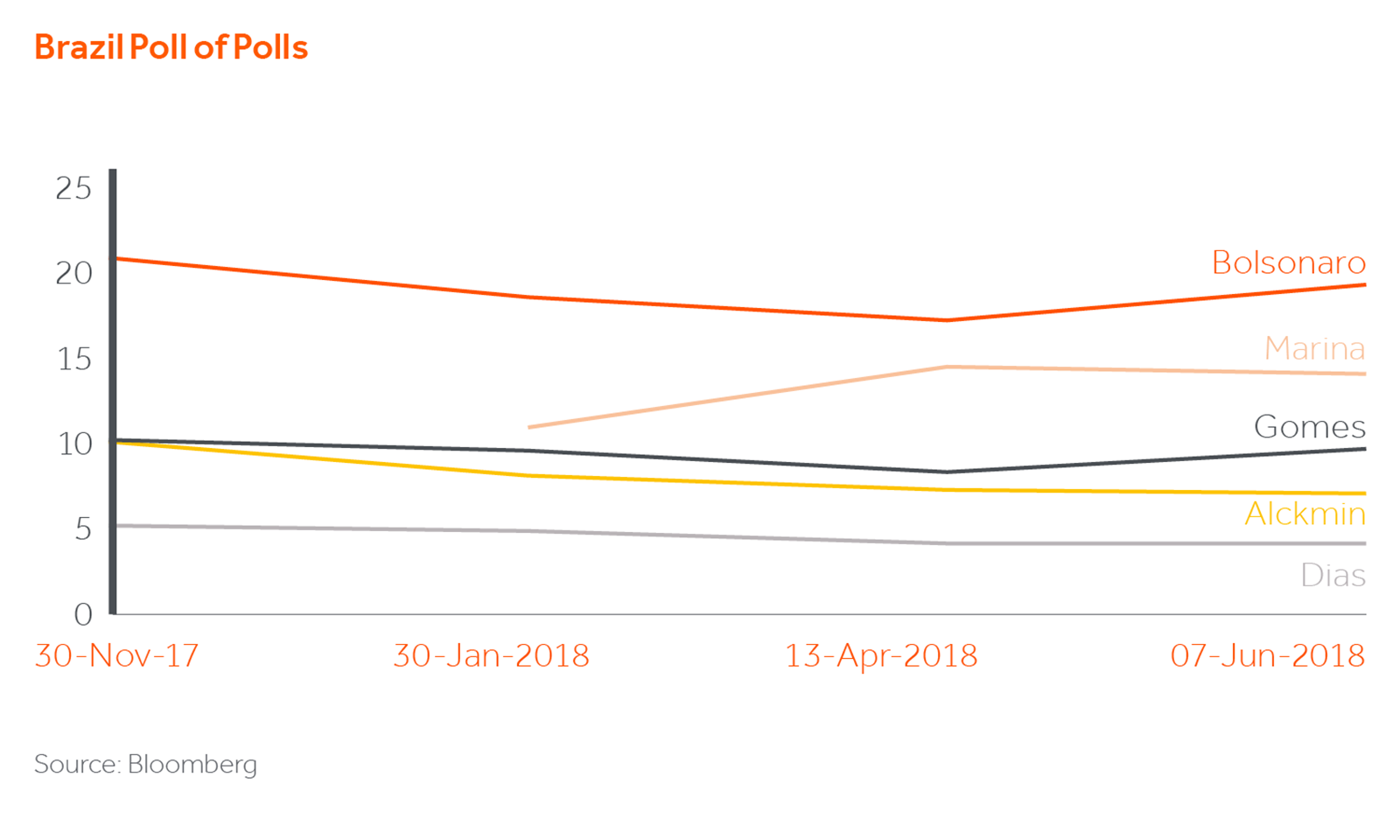

It is important to consider that in a very fragmented scenario, candidates with modest number of votes can go through to the second round and, depending on their ability to make alliances and convert undecided voters, become strong contenders. Consequently, non-establishment candidates with more polarized views like Jair Bolsonaro (right wing candidate but with unclear economic view) and Ciro Gomes (left-wing candidate) started their campaigns gathering support from relevant social/economic groups (agricultural, LGBT, religious groups).

As it stands today, according to preliminary polls, Mr. Bolsonaro holds c.19% of votes, followed by Marina Silva with c.15% and Ciro Gomes with c.10%. The center-right candidates Geraldo Alckmin (7%) and Alvaro Dias (4%) complete the list of candidates with more than 1% of voting intentions.

However, campaigns haven’t officially begun and negotiations around coalition line ups will last until the beginning of August. Most importantly, 33% of voters are blank/null. In the 2014 presidential election, the blank/null held a similar percentage but decreased substantially towards 4% during the week of first-round election, impacting the results considerably in comparison to polls released in the same week. With a more fragmented landscape, the influence of swing voters can be a game-changer. Taking a closer look at the blank/null votes, around 2/3 are undecided voters, who may form a better view through ideological and/or economic spectrum(s) during the days before the election, the remaining 1/3 are former voters of Lula, who haven’t decided which candidate they will support.

In terms of the center-right wing, which today has around 6 presidential candidates, no alliance has been officially announced. PSDB, one of the leading parties has a leadership frontrunner, Geraldo Alckmin who does not command full support inside the party. Mr. Alckmin, (former Governor of Sao Paulo State and runner up in 2006 presidential election) embodies the old politics in an environment that calls for change. Joao Doria, who is running for Governor of Sao Paulo State, started gaining support inside PSD. Mr. Doria, besides being a successful businessman, was elected Mayor of Sao Paulo in 2015 and could be the consensus/renovation candidate from the center-right with more penetration than Mr. Alckmin. We don’t expect Marina Silva, a center-left candidate who ran twice for president and was Minister of Environment in Lula’s first mandate, to tie herself into an alliance in the first round; Mrs. Silva and her team believe that the chances to qualify for the second round, without making alliances, are significant.

In spite of the uncertainty surrounding the presidential run, at least until August 15th, we see 4 candidates emerging from the first round. Bolsonaro and Gomes as polarized candidates and 2 candidates from the center including Mrs. Silva (center-left) and one consensus candidate from the center-right, theoretically from PSDB party. Fragmentation coupled with the meaningful percentage of swing voters, put an emphasis on the ability of front-runners to attract the undecided. Building consensus in both Lower House and Senate aiming at passing essential reforms is important. Brazilians yearn to elect someone that represents change, the catalyst agent in the fight against corruption and end of the Jeitinho Brasileiro (the Brazilian way).

Final remarks

Presidential elections never fail to dominate the media conversation and collective conscience in Latin America. The confluence of elections means the repercussion of such process is amplified, especially in today’s hyper-connected world.

From a social spectrum, the latinos, from Patagonia to Tijuana, have begun to nurture a zero-tolerance culture against corruption along with disillusionment with the “old” democracy. Voters, spurred by social-economic improvements achieved over the last decade are more focused on assessing the potential candidates, improving the quality of debates and increasing the level of scrutiny, which makes this an unprecedented presidential election cycle in Latin America.

The presence of candidates with more polarized approaches find support in the current scenario marked by a call for renovation and higher level of ideological debate. However, this shouldn’t be an element of disruptive change in the existing democratic system given growing institutional frameworks throughout the region.

As the region still demands investments in infrastructure, there may be bumps in the road; the changing political landscape and US rate rises have put pressure on currencies and may impact economic indicators in the short-term. However, the political tipping point that Latin American countries have reached with a more informed voting population calling for a change and mature institutions that diminish the chances of disruptive political regimes (as observed in the past), introduces a new component into the equation that will shape the future of such countries over the medium-term. Under this scenario, the improvement of economic indicators are equally important for the region, yet the idea of delivering sound economic performance at any cost is no longer an option. Otherwise, the consequences might be rather predictable, as observed by Eduardo Galeano: History never says goodbye, History says see you later.

1. The Brazilian way means finding a way to accomplish something by circumventing or bending the rules. Even though, on some occasions this approach may be associated with creativity coming from the need related to lack of support or help, the recent history shows that the Brazilian way has been translated in questionable actions and serious violations.