The world’s centre of gravity is irreversibly shifting to Asia, creating new investment opportunities and the power to define the global economic & energy outlook for the next two decades.

Accelerating the transition of Asian economies to net zero (especially scaling renewables and other low carbon, resilient infrastructure) is the single, most important lever to meet global climate targets and drive sustainable growth.

Five years on from the Paris Climate Agreement and almost two years into the COVID-19 pandemic, the benefits of reaching “net zero” emissions by mid-century are well understood for people, planet and the economy.

Smart capital is moving away from fossil fuels towards companies whose business models are based on clean electricity. The oil & gas value chain – which used to make up around 15% of the market cap across major indices ten years ago – is now less than 4%.

The oil & gas value chain – which used to make up around 15% of the market cap across major indices ten years ago – is now less than 4%.

But there are still major barriers which lock-in traditional models of capital allocation and prevent trillions of dollars from flowing out of the old, carbon-intensive economy and into assets aligned with a net zero transition.

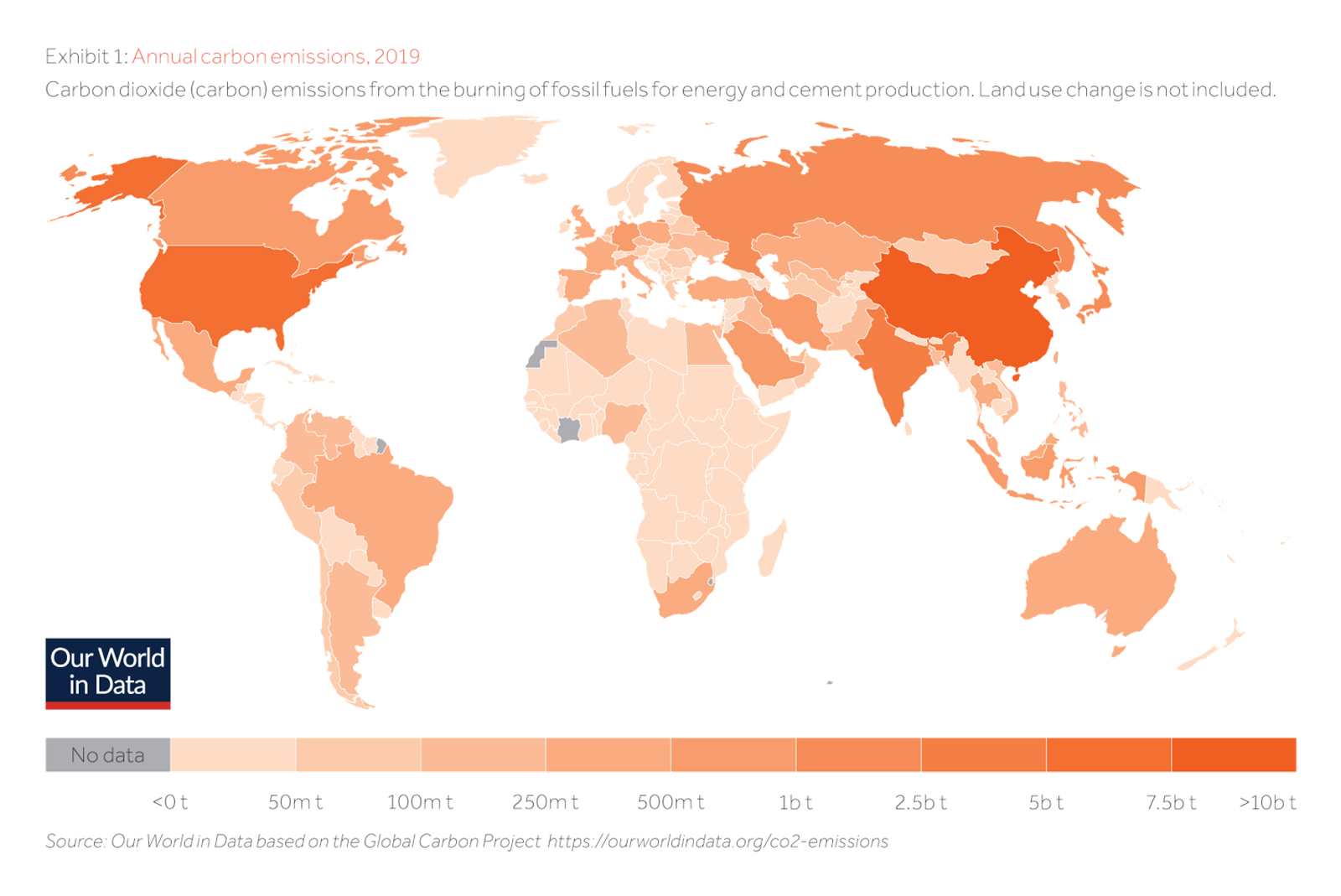

This lock-in is particularly high in Asia – which accounts for over half of the world’s carbon emissions. Without change in Asia the world will fail the climate change test.

Asia’s growth and growing climate risk

Home to over 50% of the global population and 17 of the world’s 33 megacities, Asia is also the last real coal stronghold. Over 80% of the 500 GW of global coal capacity is located in Asia and the region accounts for almost the entire (94%) global pipeline of new coal power plants.

No region in the world is more climate-exposed than Asia. Temperatures are rising twice as fast as the global average; climate-related weather events like torrential rain and typhoons are set to increase in both frequency and intensity.

While this paints a stark picture, it also represents the biggest investment opportunity of our time, especially given the growth profile of the region. By 2030, 3.5 billion Asians will be middle class. By 2040, Asia will represent 50% of global GDP. By 2050, the urbanisation rate will be nearly 65%, up from 50% today.

This growth corresponds to a massive increase in energy demand (e.g. Southeast Asia saw an 80% increase in electricity needs since 2000 linked to massive population growth, urbanisation and industrialisation). This hike in Asia’s demand for energy over the past two decades was met by doubling the use of fossil fuels.

That is no longer an economically viable course of action for Asia. As Asia is arguably the most climate-exposed region in the world, no region has a greater economic imperative to transition its high-carbon energy and industrial systems to net zero emissions by mid-century. And no region has more levers to pull to accelerate its decarbonisation journey.

Key levers for transition = major investment opportunities

The total amount of capital needed for climate-smart infrastructure in developing Asia is estimated to be at least $1.7 trillion a year over the next decade. More than 60% of that needs to come from private sector investment into assets aligned with a net zero transition including clean transport, power, water, waste management, sanitation and digital infrastructure.

As the single largest source of global temperature increase, rapidly decommissioning coal as a power source is the most urgent lever to accelerate the transition to net zero. Meanwhile, scaling clean energy in its place is the most obvious, economically viable and investable solution.

The cost of renewables is now at grid parity in most of SEA, and renewables help to tackle tackle affordability, access and energy security issues. They can also be a huge job driver, underpinning more than a third of all energy jobs and with the potential to employ millions of people, supporting COVID-19 recovery and long-term economic growth. Other than Vietnam, ASEAN countries have been relatively slow to adopt renewables.

They could do more to increase competition and strengthen the enabling environment to drive down the price of renewables, including investing in grid infrastructure, revisiting local content requirements, providing certainty around tariffs and project approvals, and strengthening PPAs.

Transitioning out of coal would also tackle major social costs linked to air pollution while mitigating the huge stranded-asset risk of fossil fuels. Climate-aligned policies have already limited the pool of investors for coal assets dramatically; soon these assets will be un-financeable.

There are other obvious investment opportunities too. Real estate and digital infrastructure are key sectors for the net zero transition: the ADB sizes the investment opportunity for green buildings in Asia at $17.8 trillion while the WEF predicts a $500 billion digital infrastructure investment gap to 2040, clearly demonstrating the scale of the sustainable infrastructure opportunity if governments can get the enabling investment conditions right.

Asia can also be a leading producer of environmentally friendly, ethically sourced wind turbines, PV modules and batteries for the rest of the world. Solar PV capacity in Asia Pacific could triple to 1,500GW by 2030: China continues to drive deployment and Indonesia is set to be the region’s fastest-growing market.

Southeast Asian countries like Indonesia are also nickel-rich, drawing in global suppliers of EV batteries and feeding the growing appetite for low carbon transport solutions.

The total amount of capital needed for climate-smart infrastructure in developing Asia is estimated to be at least $1.7 trillion a year over the next decade

Asian leaders – who have traditionally lagged on the sustainability agenda – are urgently playing catch up for fear of missing these kinds of investment opportunities

Asian opportunities, global leadership

Asian leaders – who have traditionally lagged on the sustainability agenda – are urgently playing catch up for fear of missing these kinds of investment opportunities. With Indonesia as the G20 President in 2022 and India hosting G20 in 2023, the world’s political centre of gravity is shifting to Asia, which should help accelerate climate commitments to decarbonise the region.

Of course, one size doesn’t fit all, especially in Asia’s diverse and evolving power markets. Nevertheless, the mood music is changing and net zero is now the topic du jour. China has committed to peak carbon emissions by 2030 and carbon neutrality before 2060. Japan is targeting net zero by 2050.

Indonesia’s energy utility has committed to carbon neutrality by 2050. And India is the world’s third largest renewable energy producer with 38% of total installed energy capacity in 2020 coming from renewable sources. It is also on track to become the global market leader in solar and storage by 2040.

This political leadership is driven by a growing understanding of Asia’s exposure to physical and transition climate risk, coupled with the opportunity to attract high-quality capital into low carbon sectors and net zero assets.

It will be enabled by a flourishing digital and innovation economy and should create a flywheel of enabling policies to rapidly scale renewables and support other low carbon industries.

In all of this China is key-the largest global emitter, the driver of Asian activity and at present in a deteriorating relationship with the US. Happily, though pollution is seen by China’s leadership as a pressing issue on the quality of life of her citizens.

Pathway for an Asian net zero transition

Aligning Asian economies with a net zero transition is the single most important action needed to meet global climate targets under the Paris Agreement. And getting Asia to net zero first and foremost means changing the energy mix. The Energy Transitions Commission says that it is both economically and technologically feasible to decarbonise power systems by 2040 and get to a net zero economy by 2050. Its Making Mission Possible report explains that clean electrification will be the primary route to decarbonisation, complemented by hydrogen, sustainable biomass and fossil fuels (e.g. natural gas) combined with carbon capture.

To meet these ambitions, governments, investors, corporates and civil society need to work together to accelerate the deployment of zero-carbon solutions before 2030 to put mid-century targets within reach.

Key transition pathway milestones include:

– Power sector is net zero by 2040, mainly through increased use of renewable energy

– Large reductions in energy demand across all end-use sectors by 2030 coupled with electrification of end-use sectors

– Coal for power should be reduced by 80% from 2010 levels by 2030 (coal use for power generation should already have peaked in 2020)

– Coal for power should be phased out completely by 2040, meaning:

– OECD Asian countries (e.g. Japan, South Korea) and countries in the North and Central Asia subregion need to phase out coal by 2031

– Non-OECD Asia needs to reach a reduction of coal generation of over 60% compared to 2010 by 2030 and complete a global coal phase-out before 2040

Scaling renewable energy fast enough to meet these milestones will require clear frameworks to better support deployment. For example, Vietnam is expected to add 45GW of solar PV this decade supported by feed-in tariffs and other enabling regulation.

Similarly, moratoriums on new coal like those in the Philippines can help send the right market signals. These policies will need to be coupled with commensurate support for a Just Transition, compensating workers and ensuring funding and capacity to retrain and reskill.

Ultimately, the global centre of gravity is shifting irreversibly to Asia. No other region will have such an impact in shaping COVID-19 recovery, economic stability, employment and equality and climate outcomes – especially over the next critical two decades.

That offers an unprecedented opportunity to transition the world’s energy and economic systems to be more sustainable, resilient, inclusive and investable. Ignoring this opportunity would be catastrophic for climate, capital markets and communities. Capturing it could change the whole trajectory of global growth. A prize worth chasing.