Out of the dysfunction that currently passes for US-China relations, the ASEAN economies (and those of the Indian subcontinent) have a real opportunity to exploit a recalibration of global supply chains that, both predated Donald Trump, and only seems likely to accelerate. Vietnam appears to be better positioned than most, attracting significant amounts of foreign direct investment (FDI) across a wide range of industries. However, can it continue to upgrade its productive and institutional capacities to absorb even greater inflows?

To be sure, not all production is going to move out of China despite an increasingly high cost base and burgeoning (and likely-to-be-long-lasting) trade, investment and security tensions with the US. Although there has been much wasted investment in the People’s Republic of China over the years, the physical infrastructure and intricate network of sub-contractors put in place to support global supply chains cannot be easily and quickly replicated. At least not in size with anything approaching similar levels of productivity.

Nevertheless, if even a relatively small percentage of existing production were to decide to up sticks, or marginal decisions for greenfield investments and capacity expansions were to start to move in the favour of other destinations, then the impact on smaller recipient economies would be disproportionately large. Assuming – and this is the key – that absorptive capacity can be expanded concomitantly.

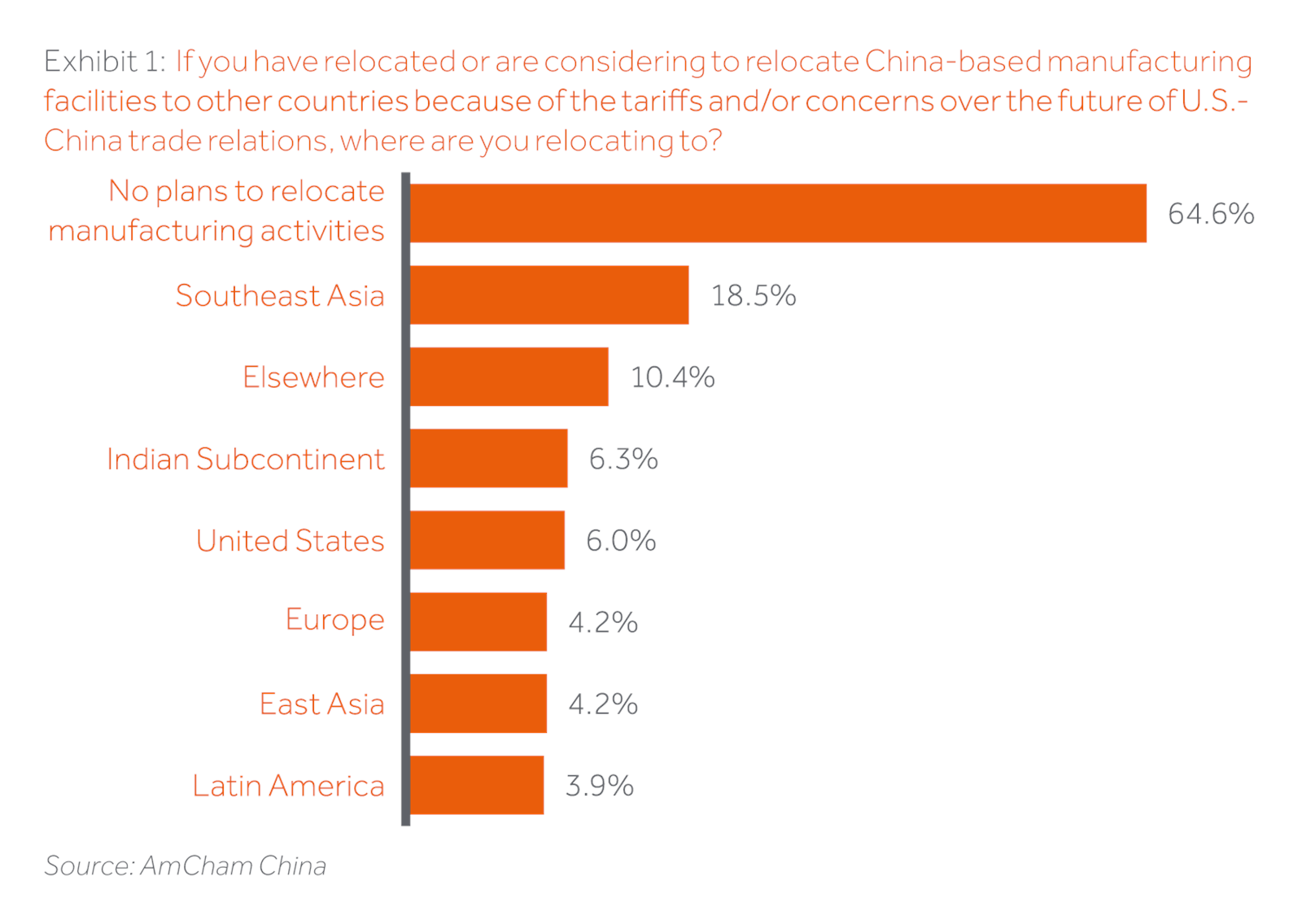

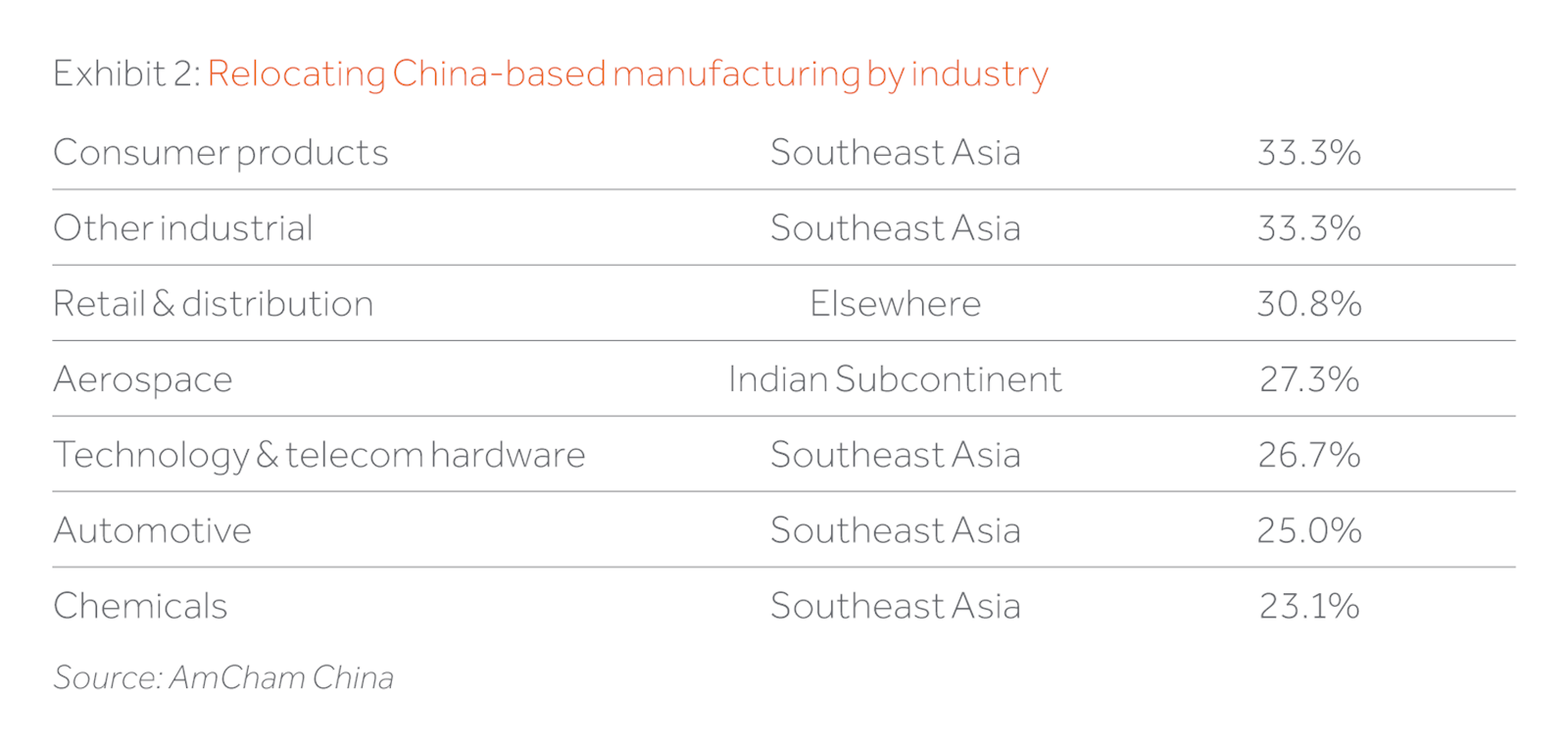

What is absorptive capacity? At the physical level sufficient provision of ports, roads, power and communication networks, as well as the ability to secure usable land for operations. However, while physical infrastructure is a necessary condition, it has to operate in tandem with the requisite human capital. This, in turn, is a function of both education, training and labour laws that while offering necessities of worker protection, also encourage companies to hire in the first place. Finally, the ease of doing business and the greater the certainty in contract and security recourse available, the greater the likelihood that long-term capital will engage. The ASEAN countries (and India) are certainly being eyed up again by potential suitors as Exhibit 1 & 2 from a September 2018 American Chamber of Commerce in China report suggests. Similar surveys of European and developed northeast Asian companies yield similar responses.

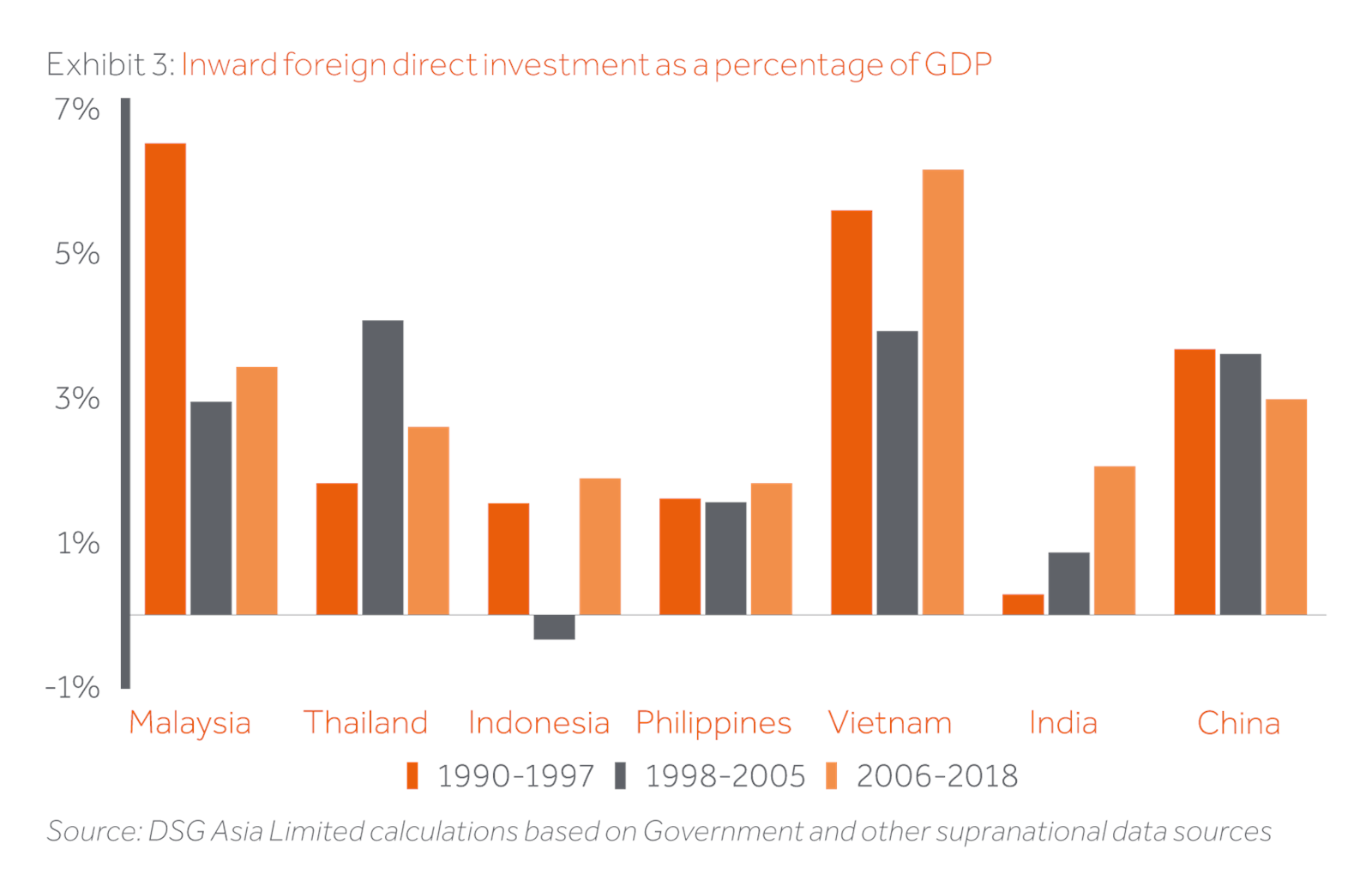

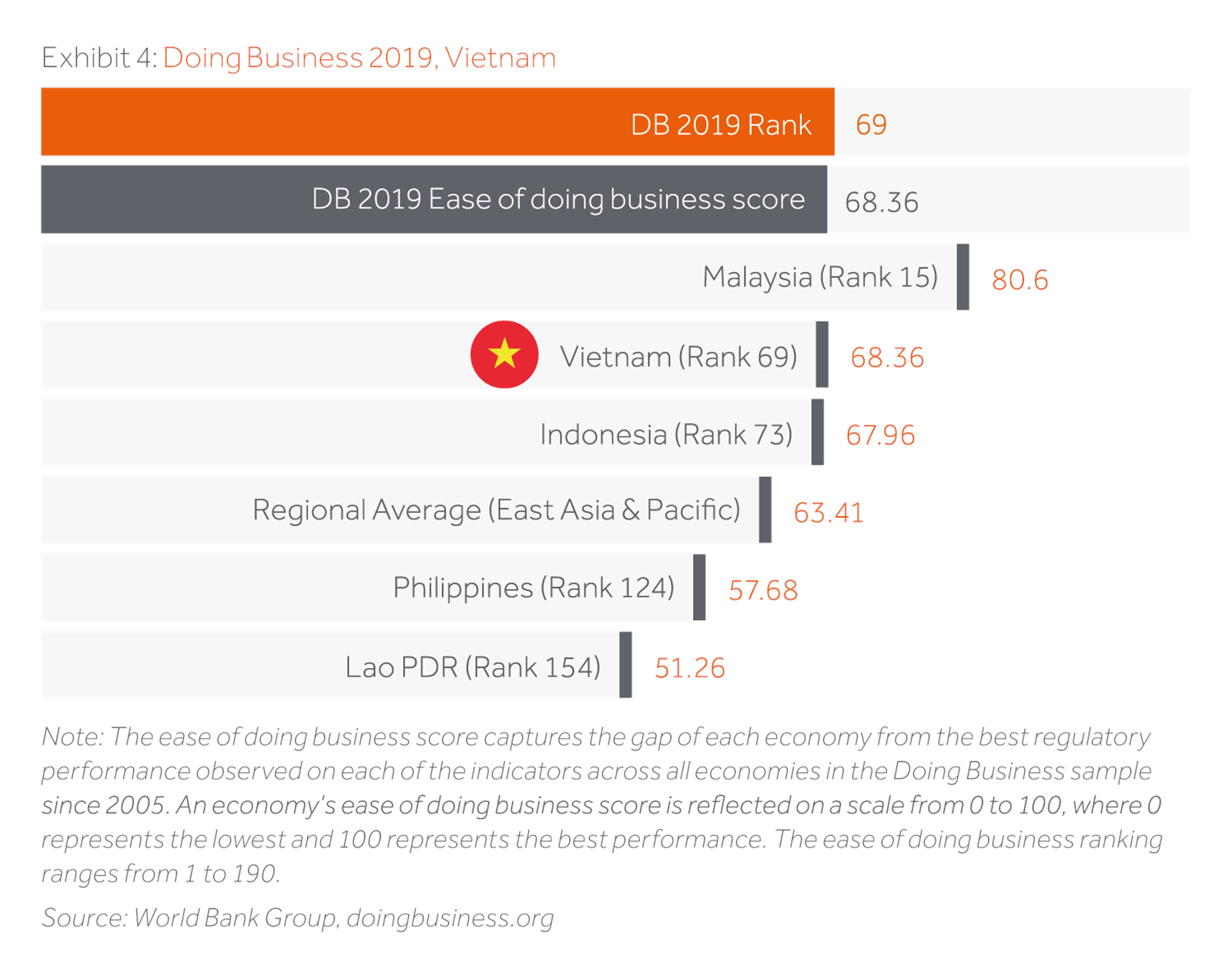

Although the survey does not detail specific country relocation plans, Exhibit 3 makes abundantly clear, Vietnam has been the region’s FDI darling for the past decade, while the country has risen sharply up the World Bank’s “Ease of Doing Business” rankings from 93rd place in 2010 to 69th today (Exhibit 4).

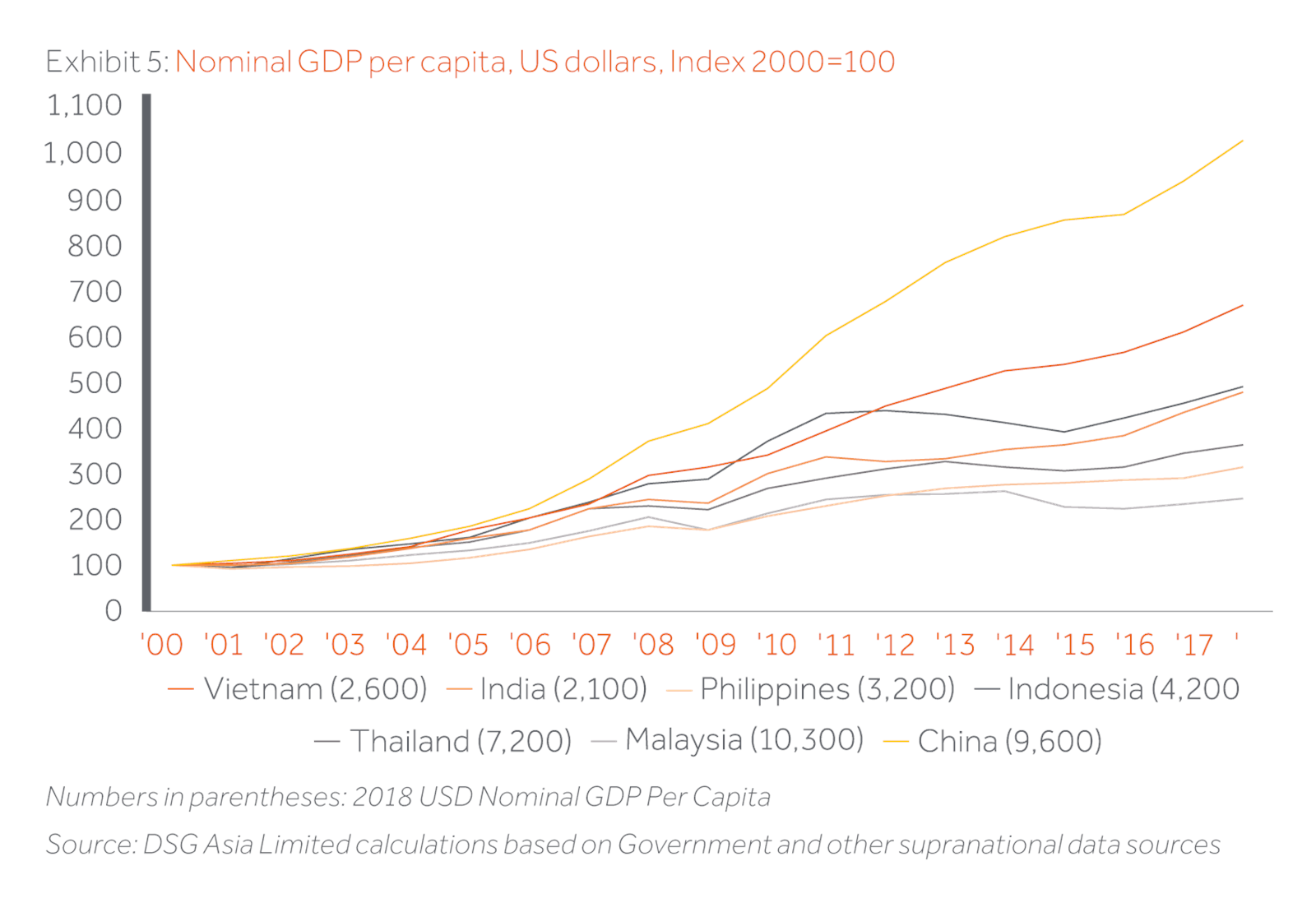

Such inflows have helped propel stellar growth rates, second only to China’s over the past twenty years. Yet because Vietnam was starting from such a low base when the Doi Moi reforms tentatively began in 1986, it remains one of the region’s poorer countries with per capita GDP less than a third of China’s. There would seem to be plenty more catch-up potential to be exploited (Exhibit 5).

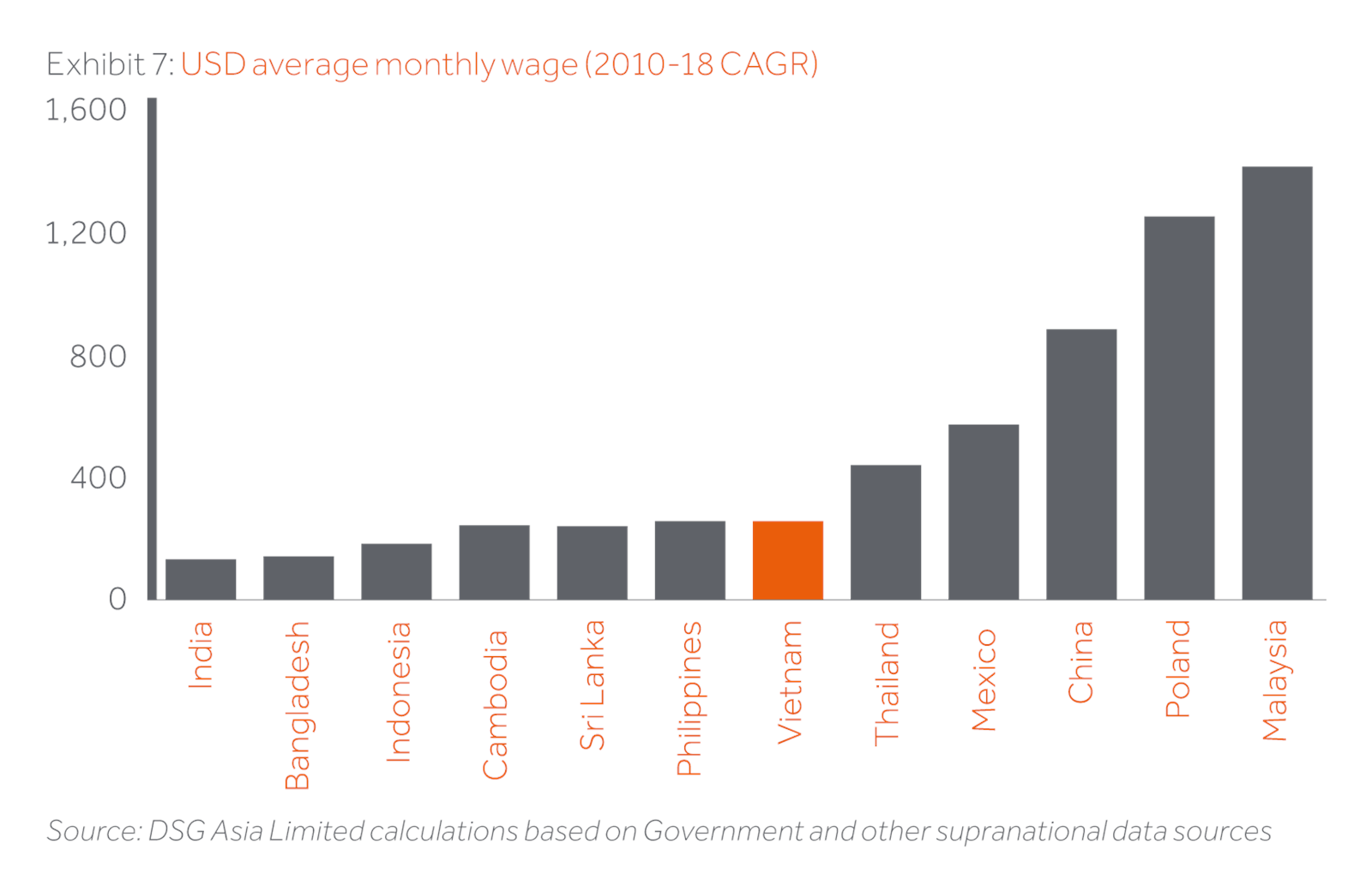

Average wages have been on the rise with companies recently reporting accelerating wage settlements and investment inflows. Nevertheless, wage levels remain less than a quarter of China’s while production volumes have risen on average at double digit rates over the last decade, suggesting that unit labour costs have remained highly competitive. Indeed, notwithstanding Vietnam’s attractive demographic profile, a greater medium-term risk may arise from burgeoning labour supply constraints – especially as demand for more skilled workers increases (Exhibit 7).

Another potential Achilles Heel is the country’s recent inability to further boost investment rates to levels that might facilitate even faster growth. A fixed capital formation rate of 25% is a more than respectable outcome but (non-bubble) rates of 30% or more have been regularly experienced by other rapidly-developing Asian economies over the decades.

There are several explanations why capital formation has been relatively moribund in recent times. Foremost amongst these is the relatively slow clean up of a lending boom gone awry a decade ago. The state-sectors ongoing outsized and distortionary role in credit and other resource allocations hardly helps as well. Subtracting FDI and public investment from the total leaves private domestic investment hovering at only around 10% of GDP. China too recorded similar private investment rates in the 1990s but the state was subsequently willing and able to create the space and conditions for this to rise to nearer 30% today.

None of this is to say that capital has not been successfully mobilised from the ground zero starting point of the late 1980s. However, capital deepening clearly has a long way to run and could be further aided by a state more willing to allow domestic private sector initiatives to flourish, and able to create greater simplicity and transparency in infrastructure procurement and delivery.

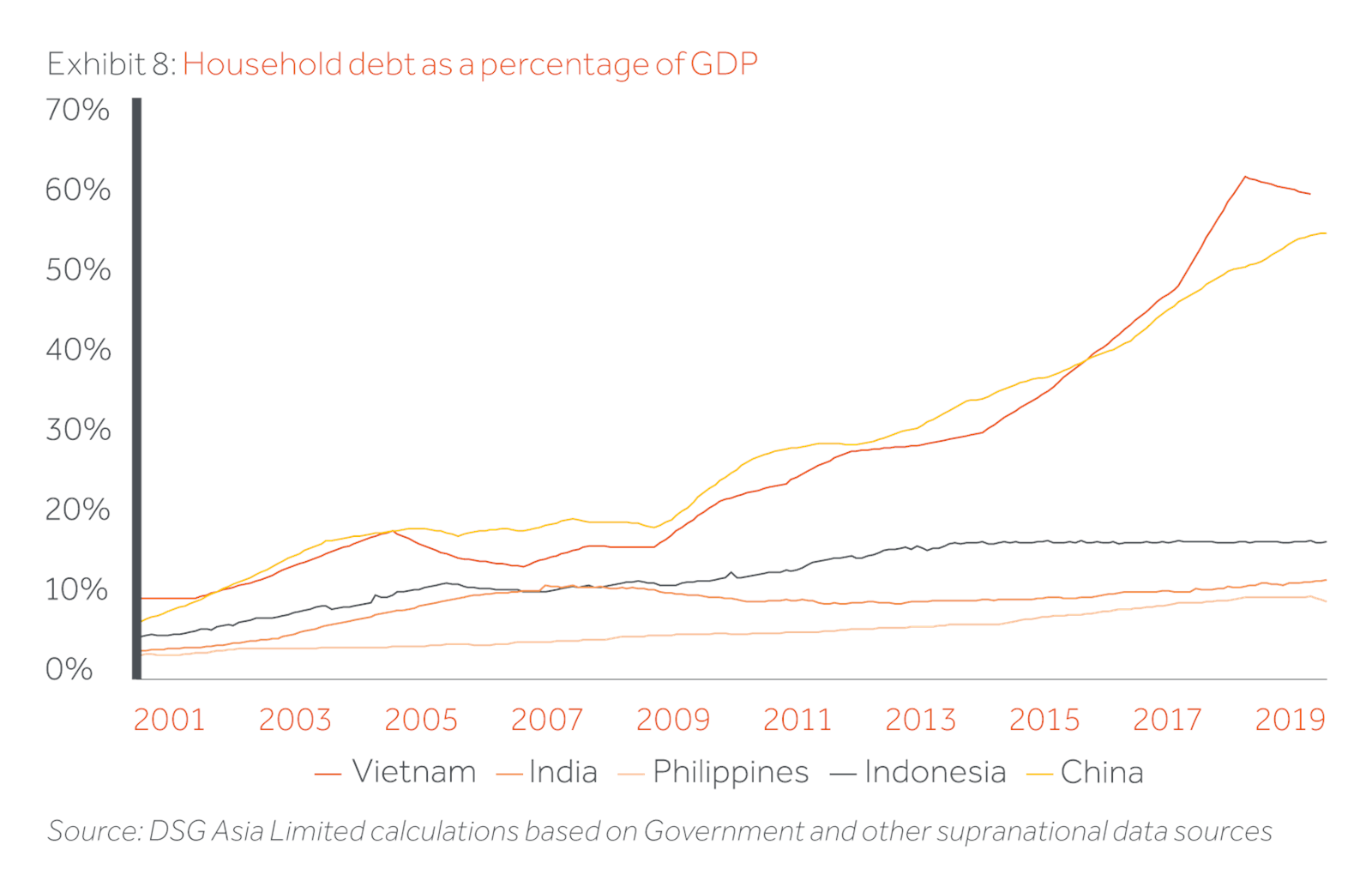

Capital markets development, which would provide alternative avenues for mobilising domestic household savings, could also potentially boost sustainable investment rates further. Currently households largely save via property since the growth of the domestic stock and bond markets remains stunted and, in the case of equities, more akin to a casino than a home for long-term investment. Households have also discovered the joys of consumer credit rather earlier than many of their neighbours and peers. Although ratios of household leverage are not yet, in aggregate, at highly dangerous levels, they do seem rather stretched for a country with Vietnam’s low average level of income. This trend will bear watching alongside the pay back between levels of corporate debt and associated returns on investment (Exhibit 8).

An over-weaning government with a strong tilt towards SOEs has arguably constrained the development of the domestic private corporate sector. More positively though, the State been willing to put out the welcome mat and has largely kept out of the way of foreign invested enterprises engaged in employment creating export industries. Such an influx of foreign capital combined with Vietnam’s young, hardworking and relatively well-educated workforce, has also allowed the country to move up the value-added chain. For example, electronics exports comprised less than 10% of total exports at the beginning of this century; they now account for a third.

Vietnam has been one of the region’s export stars with dollar shipments rising 18% per annum on average over the last decade. This aggregate figure masks a marked bifurcation though: the foreign invested sector now accounts for 70% of total exports and has delivered an annual average rate of dollar export growth since 2010 of 26%; the 30% of exports produced by domestic entities has only compounded at 13% per annum by contrast.

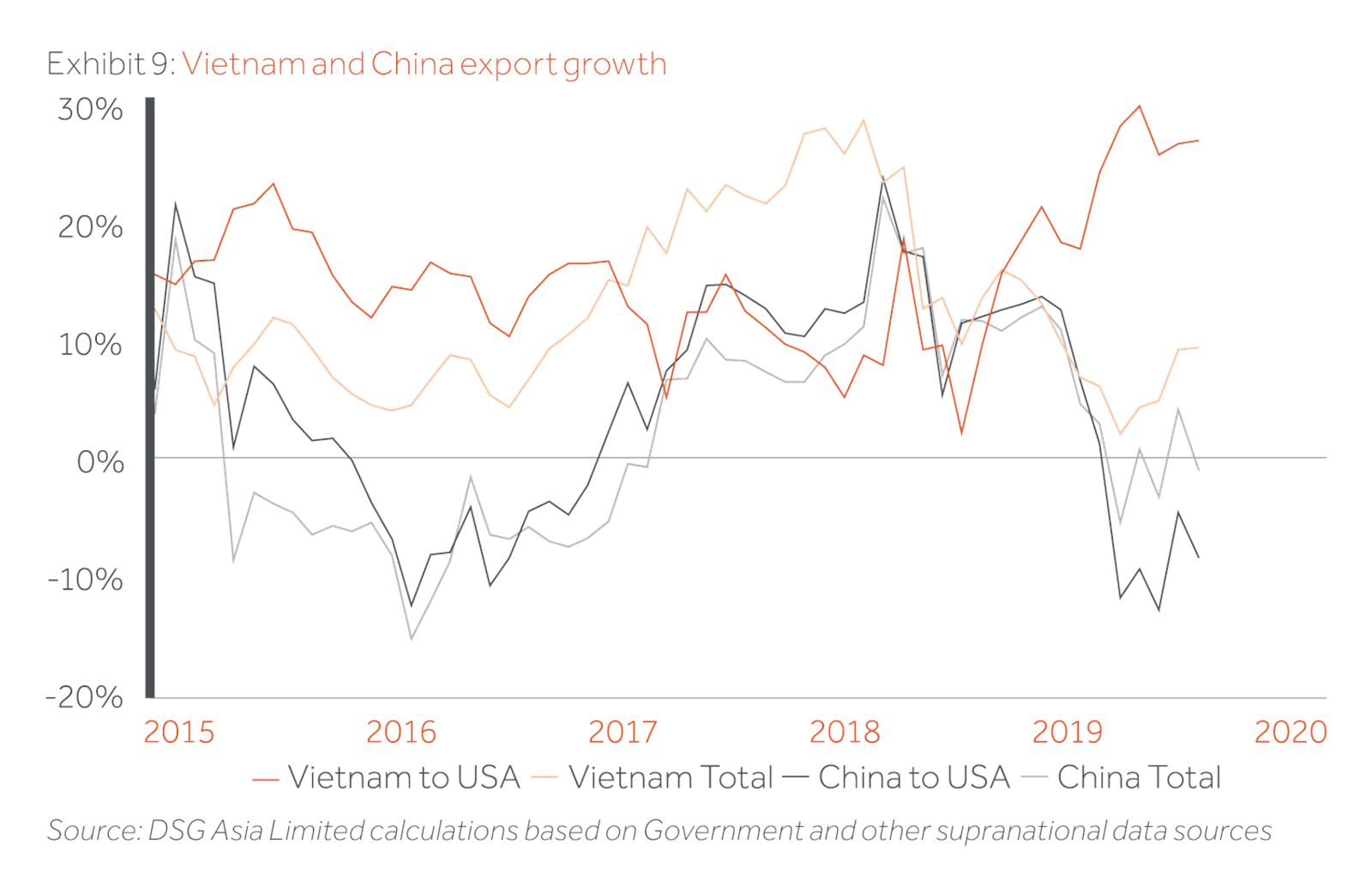

Over the medium-term, it seems fair to conclude that Vietnam has broad potential to further boost its absorptive capacity and its reputation as an attractive destination for FDI. Nevertheless, wholesale relocations of production facilities do not happen overnight and there is growing evidence that Vietnam, short-term, is also benefitting strongly from other countries re-routing their shipments, especially to the USA (Exhibit 9).

This may be a double-edged sword. 30% annualised growth of Vietnamese exports to America, while laudable on the surface, does not quite smell right and Washington is starting to train its protectionist sights on Hanoi. An overall current account position broadly in balance, and a Dong that does not ostensibly appear particularly cheap, might argue against the Trump Administration’s building accusations of currency manipulation. However, when one is dealing with a POTUS who views bilateral trade deficits as prima facie evidence of malfeasance, economic logic may take a back seat.

Vietnam can and most probably will make the grade as a fully-fledged emergent economy capable of challenging others in Asia for middle income status. But the pathway is not smooth and external issues as well as the internal challenges of regulation, margins of safety for debt accumulation and the role of the state remain important barriers to overcome in the medium term.