6) Foreign Direct Investment Matters

Foreign Direct Investment (FDI) brings in stable capital from abroad, increasing the overall investment and funding available within the country. FDI has many advantages. Long-term capital commitments are more stable and hence sustainable than short-term portfolio flows (‘hot money’). The latter leaves economies vulnerable to shifting investor sentiment and sudden outflows: Egypt is right now learning the hard way. FDI flows are also associated with technology transfer and increased export earnings.

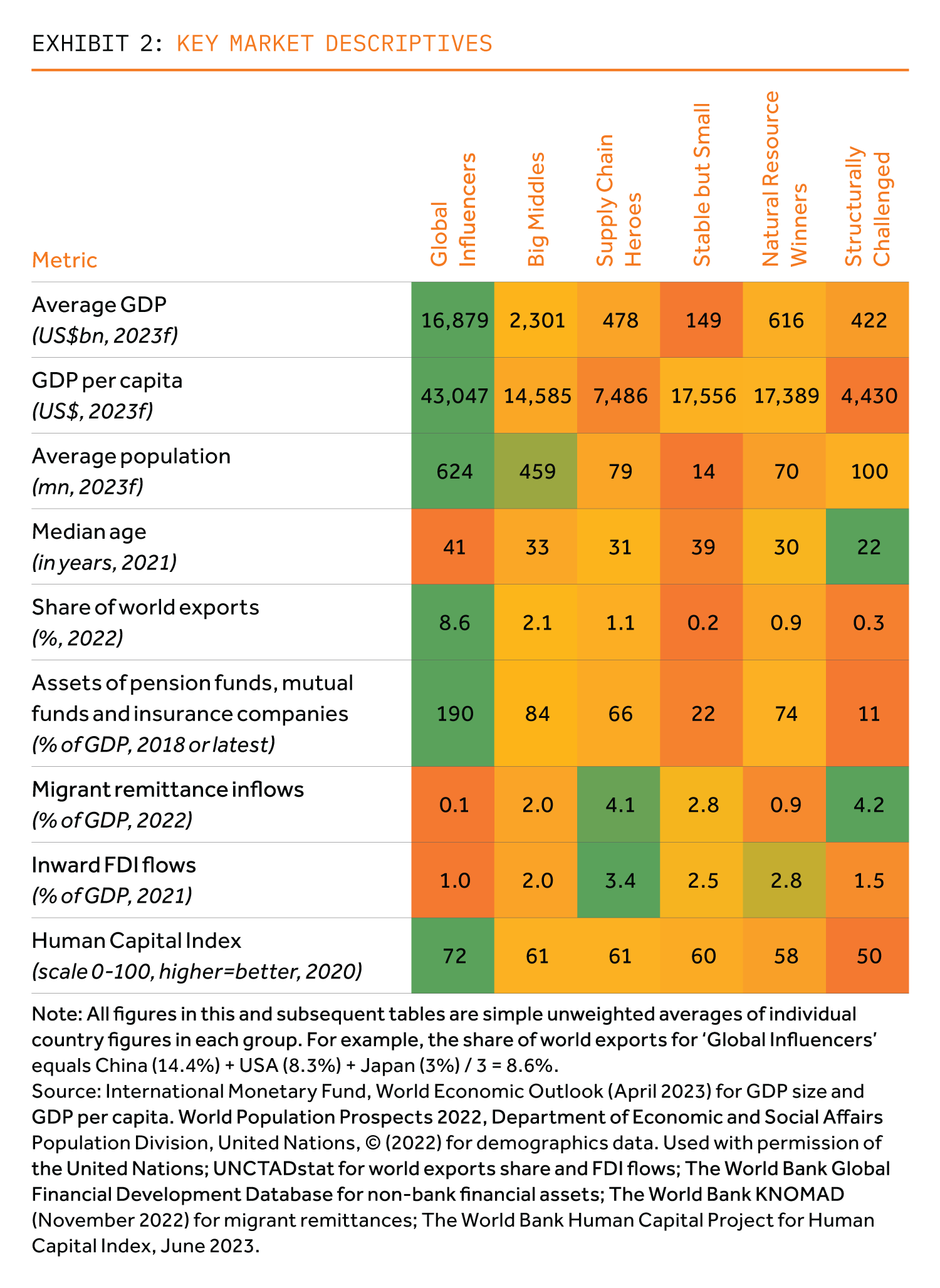

Data shows ‘Supply Chain Heroes’ are clearly also FDI Heroes. In terms of annual FDI inflows as share of GDP, ’Supply Chain Heroes’ rank as the highest, with Vietnam leading the pack across all our economies covered (5.5% of GDP). This makes sense, as FDI typically stimulates trade activities by integrating the host country into global supply chains. Foreign investors often establish export-oriented industries. Other prominent performers on this metric include ‘Natural Resource Winners’ (where FDI is linked to commodity cycles, hence more volatile) and ‘Stable but Small’. For the rest, FDI represents a smaller share of GDP.

7) Institutional Maturity Matters

Mature institutions reduce uncertainty and foster economic stability by minimising the risks associated with volatile policy changes or political interference. Institutional maturity and operational independence of economic institutions helps untie investment cycles from electoral ones. This should lead to more rational policymaking.

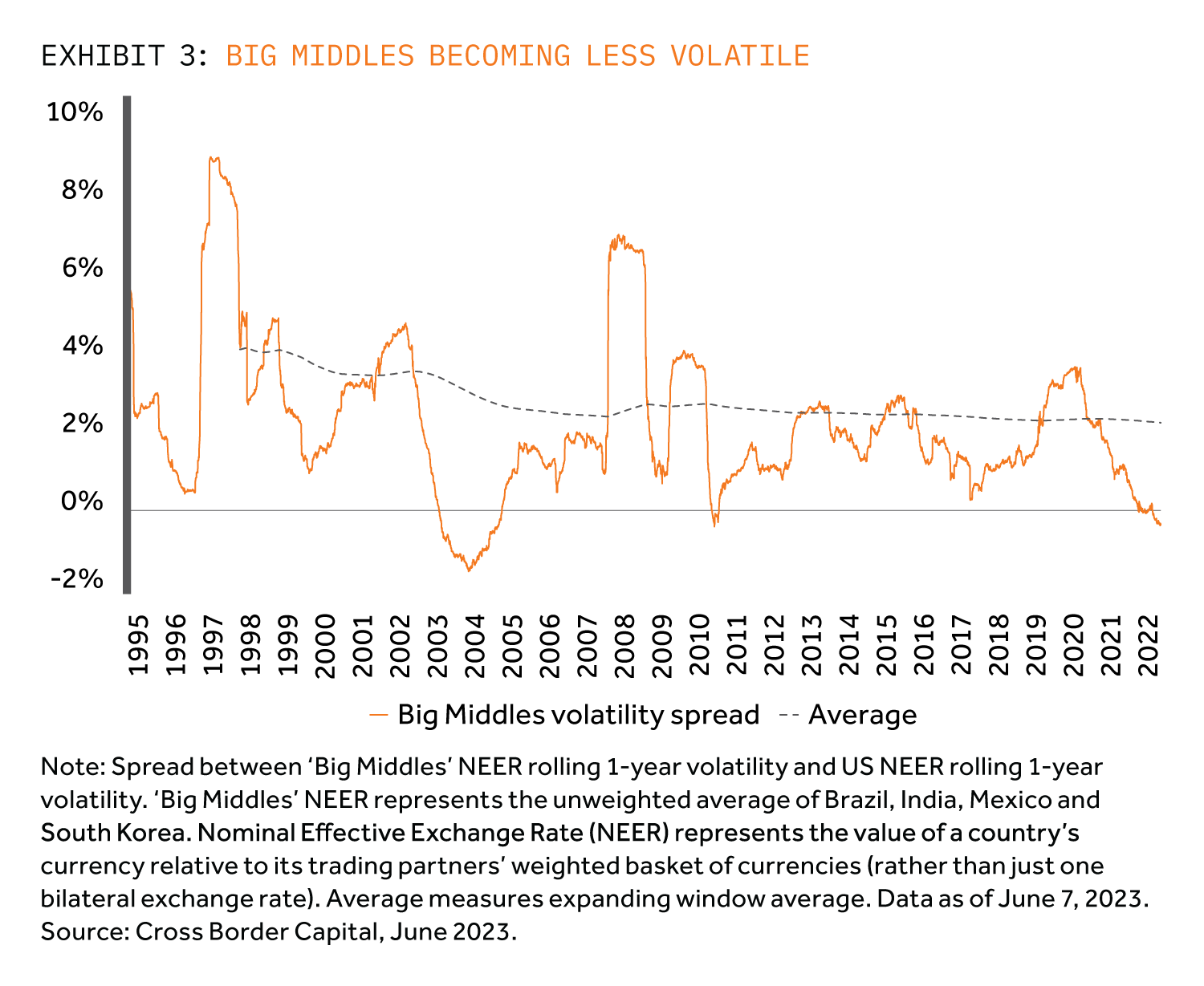

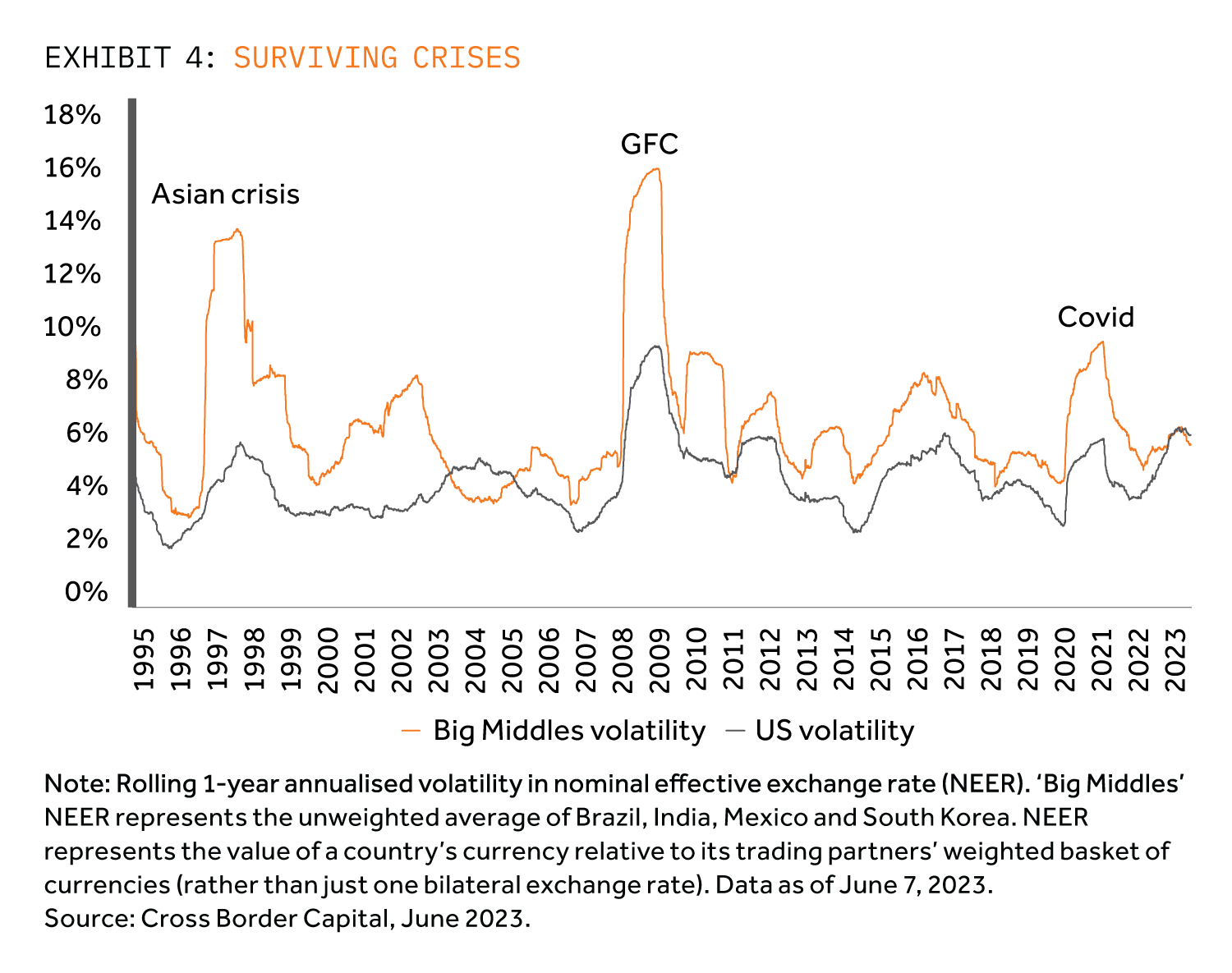

Here the ‘Big Middles’ and ‘Supply Chain Heroes’ stand out in terms of improvements. In both groups current account deficits, share of debt denominated in foreign currency and non-resident holdings of government debt are lower than a decade ago. Their central banks have become credible and independent. Countries, such as Brazil and Mexico, have been hiking prudently this cycle and getting ahead of the curve. Their economies have the largest ever FX reserves and no longer the type of currency mismatch or pegged exchange rates that have amplified past crisis (e.g. Asian Financial Crisis of 1997-98). Amongst both groups it has supported the reduction in currency volatility in the past decade and FX outperformance versus DM majors in the last years. The spread of volatility between the US dollar and ‘Big Middles’ currencies has dropped significantly in recent years (see Exhibit 3). Notably, the ‘Big Middles’ currencies have been less sensitive to extreme market events now than previously (see Exhibit 4).

To put these achievements in perspective: in the early-1990s hyperinflation plagued Brazil whilst the Bank of Thailand was a serious contender for the worst run central bank in the world (Bank Indonesia won that particular prize).

8) Human Capital Matters

The intuitive linkage between financial depth, educational attainment and productivity can be complex. We show that financial development is lowest for the ‘Structurally Challenged’ bucket, which is also characterised by lower levels of human capital development.

Looking at the World Bank’s Human Capital Index, which measures expected years of school, harmonized test scores and basic health, ‘Global Influencers’ perform the best, followed evenly by all other groups except ‘Structurally Challenged’. The relatively solid and even human capital picture across most of our investment universe is encouraging (although it masks some within group differences). It is one foundation of future economic sophistication and productivity growth.