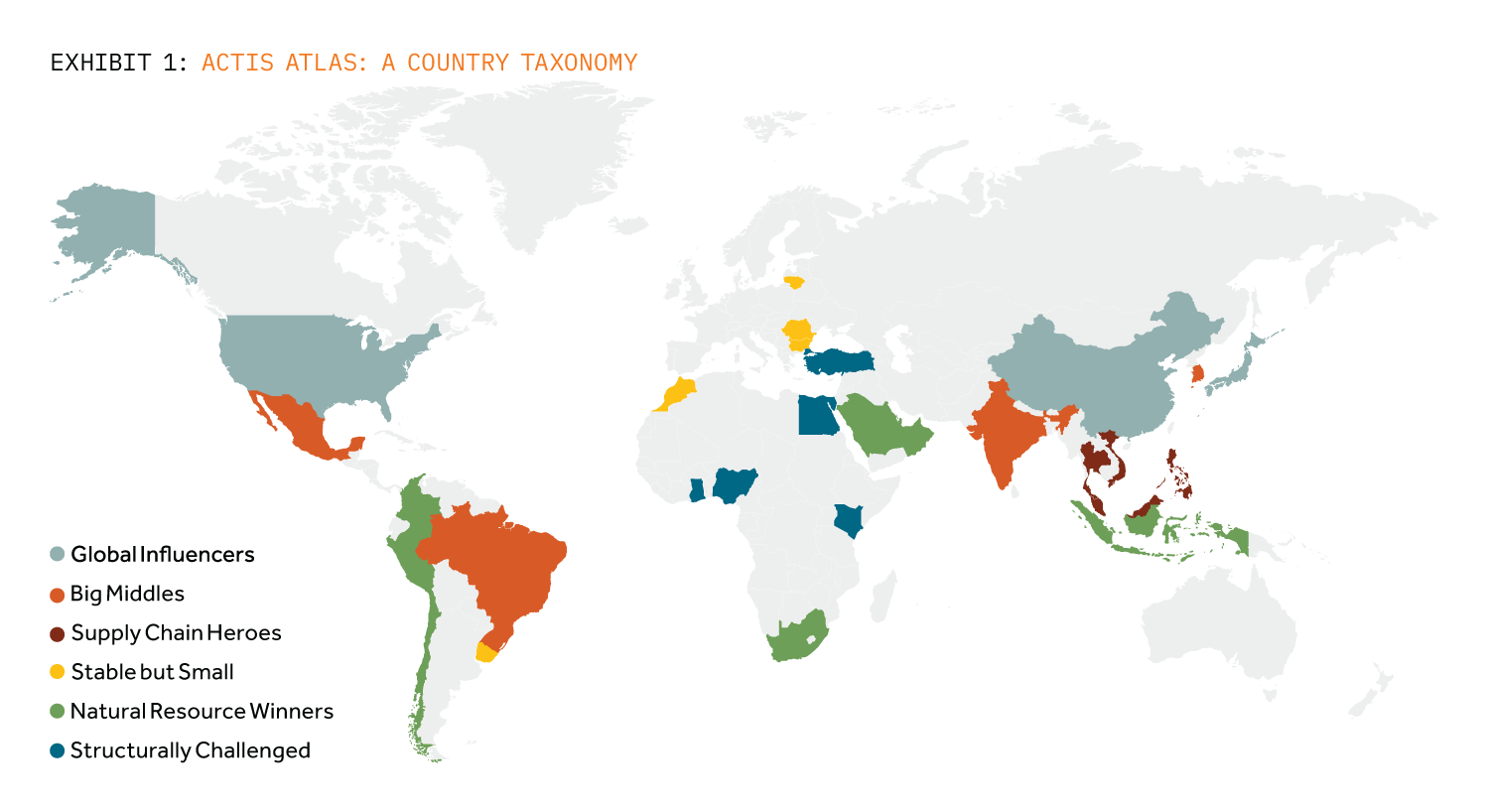

These broad characterisations have become increasingly misleading since first employed in the mid-1980’s. In this, the hand of indexation and risk budgeting hang heavy. Today, the idea of a 100-page report on the Nepal stock market as was written in 1992 (top tip Yak and Yeti Holdings) is quaint. More to the point, homogeneity has suffocated opportunity, with a handful of countries representing over 80% of most indices.

Across 80 plus countries, wide differences of opportunity are obvious. Yet common and lazy investment and media shorthand ignores this point. The weakest countries frequently dominate the dialogue. The case of Sri Lanka – a wonderful country with woeful macroeconomics – overwhelms the attractions of India just to the north in the mantra that EM is too risky, too corrupt and unable to deliver returns. ‘Four legs good, two legs bad’ to quote Snowball the pig in George Orwell’s classic “Animal Farm”.

Over the 40 years since the Emerging Markets label was first employed, other taxonomies have been tried. The investment graveyard is stacked with BRICS, MINTS, Next 11, Fragile 5 and other whims. Some struggled because the premise imploded (BRICS), others were more temporal or pejorative (Fragile 5). Most of all, the relentless march in liquid markets towards indexation obliterated incentives to differentiate. Worth noting that even the plethora of single country ETFs attract a fraction of the flows that go to the broader categorisations.

Given this, why bother to distinguish? Is there real investment opportunity in embracing diversity? We believe so.

Actis is a global investor with a particular heritage in the Emerging Markets. We have, as they say, real skin in the game. Our entire investment history – over 70 years, US$ 25 billion capital raised, and 43 countries – speaks to the value of diversity of opportunity. We are used to staring beyond the headlines to spot opportunity, whilst operating a disciplined approach to individual investment evaluation and managing risk.